| Different approaches to fx exposure, as one size won’t fit all |

back |

|

|

|

| Des Leavy of Ulster Bank sets out an approach to debt hedging strategies, and a forex exchange hedging strategy as the credit crisis continues to unfold. |

At the time of writing this in mid November, economic news flows continue to deteriorate, we’ve had confirmation that the eurozone formally entered a recession at around the same time the ECB decided to hike rates by 25bps (nice one, guys). With inflation risks easing in all major economies and the remarkably soft IG Metall wage deal of 2.80 per cent increase excluding bonus, there is nothing blocking the ECB cutting rates in December. While a 50bps cut is the most likely outcome, we can’t rule out more if the ECB feel they have lost the initiative particularly as other central banks take a more aggressive stance in cutting rates. | | Des Leavy |

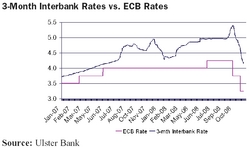

For borrowers, ECB rates are only part of the story, the dislocation between interbank rates and higher lending margins mean funding costs remain high and in many cases availability of funding is more of an issue than pricing. The graph on this page shows the absolute values of 3 month Euribor versus the ECB rate. Until markets return to more normal operation, this differential will continue to exist and will remain volatile.

Targeting the curve for value

We’re living through some of the most volatile times for capital markets in a long time. Many commentators are drawing parallels with the 1930s market crash and the resultant depression. I’m not sure where the correct comparison lies, I’m not sure it really matters, but we do need to recognise we are in a very different place than most of us have ever experienced and our behaviour needs to change to take account of this.

Protecting cash flows is more important now than ever, so is value, particularly as costs come under increasing scrutiny. In deciding an appropriate debt hedging strategy it’s still prudent to have some level of cover. We think the best value is the short end of the curve, currently you can lock in the cost of funding for two years at around 3.25 per cent or for three years at around 3.40 per cent. Not bad when you consider three month EURIBOR is setting at 4.15 per cent at the time of writing. My personal pick would be the two year rate - for a couple of reasons;

• Firstly - assuming interest is paid quarterly, then two years equals eight quarters. For Q1 the setting rate is currently 4.15 per cent. If you assume that this rate will be 50 bps lower for Q2 at 3.65 per cent, then for the remaining six quarters the floating rate will have to average 2.90 per cent before the fixed rate results in a worse outcome than if you remained floating. This seems like reasonable value. Furthermore, if you feel that the three month Euribor Vs ECB rate spread is unlikely to narrow much over the same term, then the swap is pricing ECB rates to average somewhere close to 2pct for the last three quarters.

• Secondly - there is good potential for the curve beyond two years to fall further as the market catches up with reality, by being locked in for only two years you will be able to take advantage by either tagging on additional cover at attractive levels or re-engineering any existing hedges.

We feel longer-term rates have potential to ease further. Eurozone CPI has peaked and will ease from here, the eurozone has entered recession, consumer spending is faltering, the financial system is showing only limited signs of recovering. The ECB has finally woken up and begun to cut rates. Swap markets are still pricing rates to begin rising within two years but this looks overly optimistic and before we call for rates to begin rising, we should first establish where the floor is and how long the recession will last.

For these reasons alone, five year and seven year rates still look expensive. Longer term rates probably also have room to move lower but with significant sovereign debt issues due this may limit potential. We have already seen a sharp correction - five year swaps since the beginning of 2005 ground higher over a three year period only to give back a large part of the gains over a couple of months. I don’t think this correction is over and I feel by the end of the year we may be looking at five year rates much closer to 3.00 per cent. That would be my target and if we see five years at or close to 3.00 per cent, at this stage I’d be happy starting to lock away good portions of debt. Market history is littered with long trends that end up in violent correction. EUR/USD is back where it was 25 months ago having taken just three months to undo almost two years worth of rally. Oil took 18 months to go from $55 to $145 and just four months to go all the way back to $55. I don’t see why the five year swap can’t end back at 3.00 per cent.

Longer term rates have to factor supply of government debt due to come to the market as governments seek to fund their growing deficits and cost of propping up ailing financial systems. In addition, there is growing pent up demand from corporate customers to secure long term funding and any easing in bond / swap spreads will most likely see issuance of corporate bonds. Steep yield curves look set to be a feature for the coming year. The graph on p42 shows how the EUR swap 2s, 10s spread has widened since July 2008.

In conclusion, two and three year swaps look to offer value, five to seven years have room to move lower as the market catches up with the reality of how long this recession will last. Continue to hedge but look for value in the short end and target levels further out. Beyond seven years, markets are focused on sovereign debt funding which will have to offer attractive yields to ensure successful funding.

Foreign exchange

With so much doom and gloom around, I thought I’d look at a simple trade idea that looks really attractive at the moment. This idea is for people buying EUR and selling USD. We have already seen huge favourable movements but these look to have stalled for the moment anyway. This idea is best suited to a smaller percentage of their overall exposure and ideally should be used in conjunction with other hedging strategies to give a blended risk profile. This idea is based off a current EURUSD exchange rate of 1.2500.

Target Switchable Forward

• Maximum tenor is 12 months

• Fixing frequency is monthly

• For the first six months

- Each month you buy €1 million per months at 1.2000

- There is a cap of 20 cents on the maximum gain you can make – ie. each month that EURUSD sets above 1.2000 – you buy €1 million at 1.2000 provided the cumulative gain is less than 20 cents (if spot sets above 1.2000 and the difference between the spot rate and 1.2000 is greater than the number of cents out performance remaining – you still buy €1 million at 1.2000 for that month – but the trade then ceases to exist)

- On the 6th monthly expiry date above, if the 20 cent cap has not been breached then you will be switched into the following trade

• For the second six months (50 per cent participating forward)

- Six additional expiry dates

- On each expiry date if spot sets at or above 1.2500 - you buy €2 million at 1.2500

- On each expiry if spot sets below 1.2500 - you buy €1 million at 1.2500

This gives you outperformance (up to 20 cents maximum) for the initial six months, or for as long as it lasts. If the trade still has some outperformance left at the end of six months, then this switches you into a participating forward at very attractive rates, thereby removing uncertainty after the six month term.

Many different approaches can be used to hedge foreign exchange exposures and we don’t think that one size should fit all.

Below is an example of the types of ideas Ulster Bank, CRS Ireland has access to and can deliver to institutional customers.

Automated FX trading models as a diversified source of alpha

Financial crises tend to create jumps in the correlation and volatility of financial instruments. For an investment portfolio, this often means a jump in the volatility of returns and a resultant fall in risk adjusted performance. Avoiding this impact is a challenge to all investors, particularly in recent months, but the usual rules of seeking assets with low volatility and low correlation to other assets in a portfolio still apply.

Market events over the last year and a half have brought such issues to the fore and hence the foreign exchange markets, with their high liquidity and naturally low correlation to equity, credit and bond markets, are getting more attention as a source of alpha.

Fixed allocation carry baskets, essentially passive strategies, have proved both popular and effective in recent years as the carry trade performed exceptionally well, but in the current environment the efficacy of the trade is being seriously questioned. An actively managed FX allocation provides a potential solution, but one that may be expensive and is not acceptable or available to all investors. Automated FX trading models which allocate trades based on a pre-determined algorithm are an alternative solution, which, due to their independent nature, may be distributed via a variety of products and as a result are highly accessible to many types of investor.

The recently launched RBS FX RADAR index is based on a model developed by the RBS Quant Solutions team over the last four years. Most available re-balancing models simply go long/short the highest/lowest yielding of a selection of currencies, essentially an adaptive carry trade. The strategy seeks to exploit differentials between implied yields in the FX forwards market and yields that should be expected given the risks in the currency, as calculated from a set of coefficients applied to three market observed risk factors: credit risk, market risk and liquidity risk. The size of position taken in a given currency pair is limited by a combination of currency specific liquidity ratings and an expected volatility cap on the entire position. The model re-weights monthly, and inter-month includes a function to close out the most loss making trade if the overall position breaches a peak-to-trough loss level. This underlying model is then combined with a deposit rate return to give the RBS FX RADAR total return index.

Backtested over the last eight years, the index has returned an average of 9.63 per cent p.a. yield with a volatility of 6.39 per cent. The recent extreme volatility caused the largest drawdown, but with a year-to-date return of -3 per cent and performance since January 2007 of 14.7 per cent, the index has coped well relative to other peers and asset classes during this credit crisis.

With respect to the issue of correlation jumps and the benefits of the RBS FX RADAR note to a portfolio, an excellent stress test to the diversification of a given portfolio is of course a back test on last summer’s breaking credit crisis and the subsequent after shocks. The chart below shows the performance of a portfolio consisting solely of the MSCI World index, a BRIC carry basket or the RBS FX RADAR Index. The plots of performance speak for themselves, with the RADAR model taking itself out of correlated positions and increasingly outperforming both the equity and FX carry indices as the crisis unfolds. The orange line pertaining to the right hand axis demonstrates the correlation impact vividly, as 1-year rolling correlation versus MSCI actually falls from 30 per cent to around 15 per cent during summer 2008.

The FX RADAR index is available in a variety of forms from a standard delta one product simply investing the index to capital guaranteed notes giving principal protection with leveraged access to the excess return of the index. FX RADAR, as well as other RBS indices, can be monitored on Bloomberg using RIND or on the RBS Marketplace website www.rbsm.com/indices.

Though not a central area of focus or expertise for many investment managers, the potential for high quality, low correlation returns in the medium-term through FX instruments, makes a strong case for exploring this relatively under utilised investment asset class. |

Des Leavy is head of IRD and FX Structuring at Ulster Bank Corporate Risk Solutions. (This is an updated version of an article that was originally published in FX Week in June.)

This article was published in the December 2008 edition of FINANCE Magazine.

|

|

|

|