| Foreign exchange hedge - a November case study by BOA |

back |

|

|

|

| In this case study, based on rates and forecasts applying last month, Eric Ohayon of Bank of America highlights a tailored solution for a European corporation operating in EUR, and wishing to hedge against a dollar appreciation. |

Background

Bank of America’s FX team was approached by a Europe-based corporation whose functional currency is the euro (EUR) to investigate its FX exposures. Given the nature of the company’s business, the client faced FX transaction exposures linked to a potential further appreciation of the USD.

The client’s objective was to be hedged against a potential appreciation of the greenback over the next 12 months with the added flexibility of participating in a potential rebound in the EUR/USD spot exchange rate.

As reported in Bank of America’s FX Strategy note of November 4th 2008, the bank’s forecast for EUR/USD called for a potential move higher over the next three to six months above 1.4000 before retracing to trade on a 1.30 handle. The risk however remains to the downside given the potential aggressive monetary easing going into year end.

Recommended strategies

Given current market conditions, in particular in the elevated implied volatility noted in the option market, and the client’s desire to participate in a potential ‘limited’ appreciation of the EUR, Bank of America proposed the following two strategies:

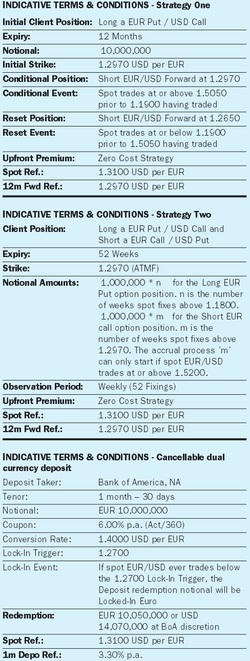

• Strategy 1 - Trigger reset

Client is initially long a 1.2970 EUR Put / USD Call option for expiry 12 months. The strike of the option is set At-the-Money-Forward (ATMF).

In the event that spot ever trades at or above 1.5050, without 1.1900 having previously traded, the client’s right to sell EUR/USD becomes an obligation (forward contract) at the same exchange rate of 1.2970.

In the event that spot ever trades at or below 1.1900, without 1.5050 having previously traded, the client’s right to sell EUR/USD becomes an obligation (forward contract) at the rate of 1.2650.

Benefits

The client benefits from a potential Long EUR Put / USD Call option position for zero cost and can participate in a potential appreciation of the euro up to 1.5050. In the event that 1.5050 ever trades, the client will be short EUR/USD forward at a rate that matches the Outright Forward at inception of the trade. Only in the event that spot EUR/USD moves straight through the 1.1900 Reset Trigger will the client be required to sell EUR/USD at the reset strike of 1.2650. At this point, spot will be trading below 1.1900 and the client will benefit from a ‘deep in the money’ position despite the reset penalty of 320 USD pips.

• Strategy 2 - Fade-in forward extra

Client is long a 1.2970 (ATMF) EUR Put / USD Call option for expiry 12 months. The notional of the Long EUR Put option accrues to the pro-rata number of weeks spot fixes above 1.1800 over the 52-week life of the trade.

Client is short a 1.2970 (ATMF) EUR Call / USD Put option for expiry 12 months. The notional of the Short EUR Call option accrues to the pro-rata number of weeks spot fixes above 1.2970 over the 52-week life of the trade. However, the accrual process, for the sold option, can only start once spot EUR/USD has traded at or above the 1.5200 Trigger Level.

Benefits

As long as 1.5200 has not traded, for every week that spot EUR/USD fixes above 1.1800, the client accumulates €1 million of a Long EUR Put option for expiry one year from the trade inception date.

In the event that 1.5200 has traded, from that moment onward, for every weekly fixing above 1.2970, the client accrues into a short EUR/USD forward position at the rate of 1.2970 in €1 million per week for delivery one year from the trade inception date. However, for every fixing between 1.1800 and 1.2970, the client will continue to accrue the notional of the long option position only.

Overall, the fader type structures are relatively flexible and allow for an easier management of the position over time. The ‘digital’ risk associated with barriers in general is greatly reduced in that it has been smoothed out over the life of the trade.

Assessment

Both solutions offer the client full protection below the current forward rate but allow the client to participate in any short dated moves higher in EUR/USD as long as those moves are not extreme. In this case ‘extreme’ moves would require the EUR/USD to trade above 1.5050 and 1.5200. Given Bank of America’s view for the EUR/USD in the coming year this represents a potentially highly profitable solution for the client if managed correctly.

In vogue - yield enhancement strategies

Given the relatively low interest rate environment, we have seen a surge in yield enhancement strategies linked to FX. Those are typically structured as deposits linked to an underlying FX transaction. The following FX Linked deposit is especially suited for investors that hold cash reserves in multiple currencies, in this case, euro and USD.

Cancellable dual currency deposit

The investor deposits €10 million for a one month tenor and benefits from an enhanced 6 per cent coupon.

At expiry, Bank of America has the right to repay the proceeds (Interest + Principal) of the deposit in either euro or USD. In the event that the redemption takes place in USD, a conversion rate of 1.4000 USD per EUR will be utilised. In the event that spot EUR/USD ever trades at or below the 1.2700 lock-in level, the bank’s right to convert the proceeds into USD will be cancelled.

The client will be assured a euro redemption for the full notional and enhanced coupon. |

Eric Ohayon works in FX Structuring at Bank of America.

|

|

|

|