| The view beyond year end and into 2010 |

back |

|

|

|

| Financial markets will remain volatile through the year end, and conditions will remain challenging next year, and even into 2010. The Head of Treasury-Ireland at Barclays Capital, Ciaran Kane outlines the approaches and products available to manage markets-related risk across currency, interest rate and commodity markets, the latter being just another area that bears continued attention, as the risk of a resurgence of oil prices indicates. |

A series of events that began with the failure of a number of specialist hedge funds in the US culminated in a number of investment banks failing or being forced into mergers adding up to a rapid de-leveraging of risk that had been built up over the previous five years. This de-leveraging has occurred in a systematic way, the most vulnerable institutions being picked off first. It started with the withdrawal of funding from specialist programmes, many linked to the sub-prime mortgage market. This rapidly spread to the main participants in these markets, the large broker-dealers, with Bear Stearns becoming the first casualty in March 2008. A period of relative calm followed before markets came under further pressure in September.  | | Ciaran Kane |

The trauma in the investment banking world then spread out across the banking system, driven by a strong aversion to non-government credit by investors. The commercial paper market ground to a halt, impacting on commercial bank funding requirements and short dated government securities fell to all time lows. At one point in October, yields on three month US Treasury Bills fell to five basis points (0.05 per cent), a clear indication that investors had such little confidence in the banking system that they were prepared to accept any return, as long as they perceived that their money was safe. We saw some bizarre situations – at one stage the cost of buying credit insurance on the US Government (the original risk free issuer of debt) exceeded the cost of buying credit insurance on McDonalds!

Government intervention became inevitable across the world, if only because there were no other funding avenues available. Various packages have been put in place around the globe ranging from guarantees of bank liabilities to the injection of capital into banks by respective governments, and in many cases a combination of both. The appropriateness of the various strategies adopted will vary based on the country, the type of institution and the market’s perception of the risk of that institution, and indeed, that country. Bank share prices have continued to fall, despite government intervention, suggesting that investors remain uncertain about the immediate prospects for the banking sector. | | Source: Barclays Capital |

While current market conditions can be described as very nervous, the actions by governments have led to a degree of stability in the money markets. A key issue for most borrowers is the significant spreads that have opened up between overnight / central bank rates and inter-bank (LIBOR) rates as liquidity in the inter-bank markets has dried up. Many corporate borrowers will source funds at a LIBOR (or EURIBOR) based rate. While these rates have moved lower in recent weeks, they have lagged central bank rates. It is likely that this situation will persist for the time being, with further pressure on rates over the year end, traditionally a period of tightness in money market rates. Significant reductions in the spreads between EURIBOR rates and central bank rates are unlikely until a degree of confidence returns to the inter-bank markets, probably well into 2009. In terms of actual levels for interest rates, we see Euro-zone rates moving to 1.75 per cent by Q2 next year - a 0.50 per cent cut in each of the next three quarters. We see GBP rates moving even lower than that with a 1 per cent cut in Q4 and two 0.50 per cent cuts in Q1 taking base rates to 1 per cent by the end of February 2009. | | Source: Barclays Capital |

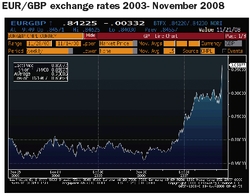

The currency markets remain extremely volatile with large daily swings in rates becoming the norm. This suggests a lack of liquidity in the market but also a reluctance amongst currency market participants to take longer term views due to the level of uncertainty. It has some interesting implications for corporates with foreign exchange exposures arising from their underlying businesses. Recent market movements in EUR/USD have been positive for USD sellers as the currency strengthens, while the opposite is true of EUR/GBP where the currency has depreciated by over 20 per cent since late 2006. While we continue to expect continued USD strength and GBP weakness in the short term, we do expect a reversal of both trends in the medium term. In particular GBP has been driven by a view that the UK economy is heading into a severe recession. While we would concur with that analysis, the reality is that the Euro-zone economy is heading in a similar direction, with a number of important economies already technically in recession. Our six and 12 month forecast for EUR/USD is 1.35 (from 1.2650 currently) and 1.45 respectively. We believe EUR/GBP will move back below 0.8000 (currently 0.8450) within six months and settle back into a

range based around 0.7700 in the medium term. | | Source: Barclays Capital |

We have seen a broadly similar story across equity markets and commodity markets. Within the trend towards weaker global equities, there has been much intra-day volatility and a lack of liquidity. The sell-off that began in the financial sector has become much more broadly based. The big story on the commodity markets has been the sharp sell-off in oil prices, from their peak at $145 per barrel in early July to $56 at time of writing. This has been largely based on a widespread slowdown in economic activity, not least from China and India. We believe that this will be a relatively short lived decline, with crude moving back into a $90 - $100 range in the first half of next year, before finishing 2009 in a $110 - $120 range.

The events of the last 15 months have wide ranging implications for corporates across their entire businesses. The financial markets related effects are compounded by the economic difficulties faced by all major economies as most of them slip into recession. This translates into a range of challenges for the corporate sector and puts a premium on a focused approach to financial risk management. Among the challenges are:

• An increase in counterparty risk. This is linked to worsening economic conditions putting pressure on trading partners, both suppliers and customers. Unusually, at this stage of the cycle, many banks have experienced difficulties, and notwithstanding the state guarantees in place, many corporates are spreading their risk across a wider range of banks than before. | | Source: Barclays Capital |

• An increase in borrowing margins as banks start the long (and inevitably painful) process of re-building balance sheets. This situation is exacerbated by the capital position of many banks which means that new funds for lending will be less freely available than in the past. This situation will only be resolved when banks raise fresh capital. While we have seen some progress in this area in the US and the UK, much of it driven by governments, it remains an unresolved issue in many European countries. It is unlikely that this situation will improve materially in 2009 so access to funding, even at historically unattractive margins, will be important for corporates seeking to grow businesses or make opportunistic acquisitions. It also underpins the importance of strong relationships with a core group of banks who the corporate can utilise as a source of advice as well as funding. | | Source: Barclays Capital |

• Increased volatility in foreign exchange markets can be a source of increased risk in relation to existing hedging policies. The setting of budget rates become a much more precarious exercise, as does the risk that the ultimate outcome a year later is significantly better (or worse) than the budget rate, ie. it introduces a lot more uncertainty into the business model. It should also cause corporates to look at how they hedge, for example the opportunity cost of using FX forwards in an environment where rates subsequently move significantly in their favour. An alternative is to look at a range of option based solutions that protect their downside but give varying degrees of participation in the favourable rate move.

• In relation to interest rate markets, the recent turmoil has seen central banks move aggressively to cut rates and put inflation concerns on hold. These inflation concerns are likely to diminish greatly as the economic slowdown impacts on pricing levels in all sectors. Central bank rates have further to fall, albeit that the outstanding issues with LIBOR rates outlined above will take some time to resolve. Longer term fixed rates in the Euro-zone are about 1.50 per cent off their peaks and will likely fall further into the first half of 2009. Corporates looking at attractive levels to fix longer dated interest rate exposure should consider hedging opportunities that are likely to present themselves from Q2 2009 onwards.

• An area that has captured less attention in the recent turmoil, but remains a real source of risk to many corporates is that of commodity exposure. There are now many potential hedging solutions available across a wide range of commodity products and in an over the counter format that will suit the requirements of a corporate seeking to hedge. Commodity hedging has seen increased corporate activity in recent years, a trend that is likely to continue.

Market conditions will remain challenging well into 2009 and possibly into 2010. The restoration of confidence in the financial system will take time, but it will happen. This returning confidence will lead to a more liquid inter-bank market, falling LIBOR rates and stronger bank balance sheets. A healthy banking system is essential for the resumption of economic growth in all economies and the role of both governments and regulatory authorities will be critical in assisting with this process. Many of the challenges facing corporate treasurers and finance directors in the months ahead will be unusual in that they may not have been faced before, but they are not by any means insurmountable. |

Ciaran Kane is Head of Treasury - Ireland at Barclays Capital.

|

|

|

|