| Financial weapons of liquidity and transparency: credit derivatives after the credit crunch |

back |

|

|

|

| Professor Moorad Choudhry explores the interconnection between credit derivatives, including structured credit products such as collateralised debt obligations (CDOs), and the 2007 sub-prime mortgage crash and subsequent credit crunch. He discusses how the age-old adage of investing, to know one’s risk, remains as important now as it was in the time of the South Sea bubble. He suggests further that credit derivatives, far from being in some way instruments of evil, are vital to maintaining liquidity and transparency in the financial system. |

Corrections in financial markets are nothing new. All students of economics are familiar with the South Sea bubble, the Dutch Tulip bubble, the Wall Street crash, the 1973 oil-price hike and the Latin American debt crisis. Like the business cycle generally, they are an inevitable part of the market economy, which is what they have in common. What they also have in common is that they didn’t exist in an era of financial derivative instruments, famously referred to as ‘financial weapons of mass destruction’. We conclude therefore that it is as possible to lose money spectacularly in cash markets as it is in derivative markets. Put another way, one doesn’t need derivatives to make the wrong investment decision and lose money as a result.  | | Moorad Choudhry |

The current crisis

The origins of the current crisis are rooted in a number of factors, including some less obvious ones. Globalisation and the interdependency in financial markets made mortgage defaults in the United States translate very quickly into large-scale banking losses around the world. Low interest rates and a positive economic environment fed the origination of mortgage assets and their inclusion in structured finance products, as investors worldwide sought higher yields. The investment decision often considered the credit rating and nothing more.

All this has been reported in the business media, with the emphasis in a populist agenda focusing on the search for scapegoats. Less evident in the media reaction has been any comment on the old-fashioned mistake of poor asset allocation. We have heard less about flawed investment analysis and decision making, and more about the evil of structured credit products and the incompetence of rating agencies. But in any institution, it is the former that really leads to losses, not the latter.

Know your risk

Smarter investors were aware of the impending fall-out in the US housing market ahead of the crash in asset-backed commercial paper (ABCP) markets in August 2007 (generally regarded as the ‘start’ of the crisis). A small number of banks and hedge funds shorted the US sub-prime market in 2006-2007, and consequently made super profits as the downturn proceeded. They did this by buying protection on sub-prime assets using CDS of ABS, credit default swaps written on asset-backed security tranches. Credit derivatives enabled these firms to generate profit in a bear market, a truer test of skill and ability than the majority of structured credit desks in Tier 1 banks that booked large profits in the boom years, only to hand them all back after the crash.

In the booming economic environment of 2002-2006, the search for yield became urgent. Investors sought in effect a ‘free lunch’ as they bought investment-grade rated ABS and CDO securities priced to yield more than equivalent-rated corporate and sovereign securities. In the market downturn, they failed the Number 1 test of any investor: to know their risk. How many investors actually checked the credit rating agencies’ rating methodology, which drove the credit ratings assigned? The ones that did would have realised that the underlying approach to valuing (and hence) rating ABS and CDO securities, based essentially on the one-factor Gaussian copula model, contains a number of parameters that are set using assumptions. One of these parameters, default correlation, is not even an observable statistic. Another parameter, the recovery rate, must be assumed, when in practice it ranges from 10 per cent to 90 per cent.  | | Figure 1 |

A difference of opinion is what drives markets. Without a difference of opinion there is no liquidity. If investors were sceptical about the rating methodology, they were always in a position to not agree the valuation, or demand a higher premium for holding the securities. Or simply not buy the securities. That they did not, but then sought a scapegoat after suffering the consequences of their own investment decision, speaks volumes. Rather, investors looked at AAA CDO or CDO of ABS securities paying anything from 20 to 50 basis points more than AAA sovereign securities and piled in. But this difference in credit spread existed for a reason, namely that higher-paying securities reflect greater relative risk. Little thought was paid as to what the CDO or ABS bond’s underlying assets were, or as to how the mark-to-market valuation of the CDO tranches changed with changes in exogenous factors and could fall even without a large number of underlying defaults. As the first defaults started to feed through from the sub-prime market to ABS and then CDO bonds, the overlying securities were downgraded, which resulted in mark-to-market losses and consequent write-downs.

A clear lesson from the current crisis is ‘know your risk’. Equally, it is to be wary of piling into the market following an extended bull run. It is not to avoid securitisation, structured finance securities or credit derivatives. To do that would be to throw the baby out with the bathwater.

Structured credit products: the future

The simplest credit derivative, the CDS contract, is an elegant and accessible instrument. It allows banks to transfer credit risk exposure (to other banks) and so better manage credit risk; equally, it allows investors to have a synthetic investment in an asset class that does not require funding. The idea that the CDS is somehow to blame for this crisis is a nonsense that we don’t need to address for even a moment. Rather, it is worth considering how the liquidity available in CDS prices now makes them an efficient indicator of market sentiment and relative value. The transparency available in CDS far exceeds that in the cash market. We illustrate with the Morgan Stanley CDS price at Figure 1; observe that the price spikes up ahead of the Lehman default; after the default it spiked again. This showed unambiguously what the market thought of that reference name as the crisis reached its peak.

What we have observed in the credit derivative markets in recent years is a repeat of what occurred in interest-rate markets a generation ago: the derivatives tail wagging the cash dog. For a more accurate and instant indicator of relative value, market participants consider the CDS price ahead of the cash asset swap spread. Credit derivatives are now the key valuation indicator and will remain so because of their liquidity and transparency. Investors wishing to access any name should always consider both the cash and synthetic market in the asset, and conduct their decision analysis with recourse to both markets.

That is not to say that problems in areas such as documentation and back office settlement do not exist; there is patently an issue here. But that is connected with the development of an efficient operational market, and not to decry the advantages of this product class in principle.  | | Figure 2 |

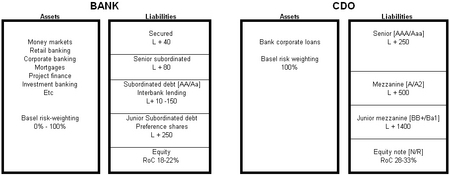

A more complex credit derivative such as a synthetic CDO is nothing more than a mini-bank. We show this at Figure 2. The asset-liability profiles are remarkably similar. Just as investors can decide whether they want to be at the extreme end of a bank’s risk-reward profile, by holding its equity, or at the lowest risk investment by holding the secured debt, so they can also decide whether they want to hold CDO equity or a senior tranche. In either case, the asset will be marked down in a market correction, as we are seeing now. Of course secondary market liquidity is higher for bank-issued securities than CDO securities, which is an issue for consideration. But the underlying fundamentals are identical. The product itself is not the source of losses; rather, profit or loss is a function of the quality of the assets in the vehicle – be it bank or CDO. For an investor to blame losses on the CDO and state that it is a bad product is as valid as saying that a bank is a flawed “product” that causes losses.

The benefits to financial markets and the global economy of securitisation and credit derivatives are obvious and, in the case of ABS, of long-standing. The advantages are still being derived now, albeit not in the traditional sense. Currently banks are combining credit derivatives with securitisation technology to undertake Basel regulatory capital relief trades over the year-end. These are in effect short-term securitisation transactions. The banks do not need to find investors for cash ABS in this instance, but merely trade in the wholesale banking markets. This is a further example of the product class aiding more efficient bank balance sheet management.

Conclusion

The ability to transfer credit risk, whether by CDS or securitisation, will always be important. In a market of greater investor confidence, the search for yield will mean that ABS securities will be in demand again. No-one would seek to predict a time when the market upturn will begin, but one prediction we can make safely is that investors will not be happy to hold T-bills for ever. When that time comes, structured credit products will be at the forefront of another bull market run. |

Dr Moorad Choudhry is Head of Treasury at Europe Arab Bank plc in London and Visiting Professor at the Department of Economics, London Metropolitan University.

|

|

|

|