| Credit risk and the pricing of mortgage products |

Back |

| The economic climate has resulted in lenders offering more and more competition to borrowers looking for a mortgage. As the European Central Bank (ECB) has successively raised interest rates, so consumers have begun to see the advantages of switching mortgages. Professor John Cotter argues that, as the economic outlook changes, the key is getting the right price both for the lender to be profitable based on their risk assessment involved and also represent a competitive and attractive price for borrowers. |

House prices have been the talk of the town for the last decade (and certainly are up there with weather talk). We have seen large levels of house price inflation that has levelled off in recent times and it is the magnitude and staying power of house price rises that has caught our attention. More recently we have also seen enormous coverage of the role of credit risk, and in particular, the collapse of mortgage (sub-prime) markets due to extreme negative market realisations.

In this article I am going to discuss Irish mortgages focusing on the drivers of supply (banks) and demand (house buyers) and the resulting overall market. Also I am going to discuss credit risk for mortgages and focus specifically on the Irish market. Unlike the mortgage stories coming from the US and elsewhere, this is a much happier story.

Let us begin by focusing on banks. Banks impose different prices on their spectrum of loan and deposit products and we know this can be a highly profitable business assuming adverse selection is avoided serving both the interests of borrower and lender (for instance, without banks, the borrower faces a problem of how to get a loan organised).

For every loan the bank must decide the price (interest rate) they charge for it. Essentially banks do not consider every Euro lent to be the same. They price the loan based on the credit risk of the borrower. And if you take two borrowers with different credit risk then the bank charges diverging interest for the same euro lent.

Credit risk

So the banks incorporate credit risk in their loan pricing. Why? Well credit risk is made up of two elements – the probability of default times the size of default. Thus higher credit risk implies a higher potential for default for a given euro and/or a higher magnitude of default for a given likelihood. The idea of banks incorporating risk in their loan pricing is based on the principle that the higher the credit risk the higher the price (interest rate) charged on a loan. Banks have a number of methods to determine the probability of default and they weight that by the size of the loan giving a measure of the uncertainty associated with the loan.

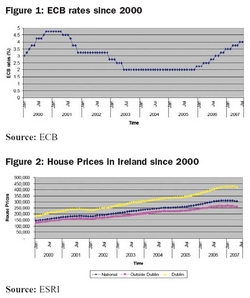

However, banks are constrained somewhat on the price that they charge for a mortgage as they charge a margin over the ECB rates. What we have seen here is that interest rates have (from an all time low) steadily increased in the last couple of years. In fact the rate increases are now talked about as much as house prices themselves recognising the importance of interest rates (price of money) to the Irish property market.

From the graph chartng ECB rates since 2000, it is clear that the cost of borrowing has increased substantially in nominal terms as a result of increasing ECB rates. Thus for every Euro borrowed the repayment costs have increased substantially. This has concentrated borrowers minds on the interest rates of loans and much analysis is done under of realm of personal finance trying to identify the optimal mortgage products in terms of price.

There is little formal analysis of the impact of changing interest rates on the cost of borrowing in the Irish mortgage markets. An exception is the EBS/DKM affordability index that examines first time buyers. Although this group has seen an improvement in affordability recently as a result of stamp duty and related tax changes in December 2006, prior to this average affordability had worsened by approximately 30 per cent since 2000. In contrast, affordability for non-first time buyers did not benefit from the budget changes in December 2006.

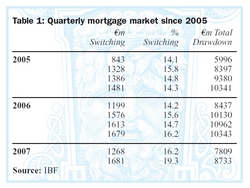

Second, house prices have shown massive increases over the last decade and slowed down in the last year (coinciding with the increasing ECB rates and other micro factors such as stamp duty arrangements etc). We can see that houses prices more than doubled since 2000 throughout the country coupled with recent stagnation. While it is difficult to predict what will happen to house prices going forward most commentators are staying away from predicting the sort of growth experienced since 2000.

Third, the operations of the mortgage market are becoming more flexible. Now more than ever it is possible for borrowers to not only recognise price differentials for available mortgage products, they can also exploit these by switching their loan from one provider to another. To illustrate, we can see the magnitude and market proportion of mortgage switching in recent times. Clearly switching is important. In fact it has more than doubled since 2005 (according to Irish Bankers Federation/ PricewaterhouseCoopers, 2007, IBF/PwC Market Profile).

The prediction is that switching between lenders will become even easier with reduced administrative costs (eg. the main current costs relate to conveyancy fees and the proposed introduction of e-conveyancy would dramatically reduce the associated costs of switching).

Looking forward

Given our brief outline of the characteristics of the new Irish mortgage market facing banks and borrowers at present, what can we say about the overall picture of the market at present? Also can we make any comments on the market going forward?

I think it is clear that the main market is in existing mortgages and that price competition there has started to make a serious change to the market’s overall structure. This will evolve even further in the future. We can see that drawdown levels have dropped from 2006 to 2007 (although the composition of this drawdown is also changing). To use a food analogy, the pie is not getting bigger, but the ingredients are changing. Thus price competition based on, for example, credit risk analysis, will result in more suitable products being developed that are attractive to borrowers.

A positive example can illustrate the point; Last year National Irish Bank launched a new mortgage, the Loan to Value (LTV) mortgage, that has been very successful and spawned a number of very successful copycat products by its competitors (for analysis see Cotter, 2006). These related products were underpinned by using credit risk to delineate borrowers according to the equity built up on the mortgages due to increasing house prices. For instance, it is easy to see that an average house on a 100 per cent mortgage given out in 2003 had by 2006 obtained a LTV of 60 per cent. Those borrowers would now have lower credit risk than those on 100 per cent mortgages and would be charged a different (lower) rate.

Overall these new products have resulted in a more competitive market for mortgages and are essentially a ‘win-win’ situation for borrowers and lenders. The borrower faces lower repayments (especially during a time when repayment levels are starting to gravitate upwards) and the lender increases the value of their loan book. This change is underpinned by innovative pricing of the credit risk associated with borrowers where banks have used their financial expertise in developing attractively priced products.

Conclusion

Given potential increases in the ECB rate in the future (and certainly a flat if not upward sloping term structure of interest rates) we should start to see further success for products like the LTV that suit both lenders and borrowers. This is especially true if the levels of new mortgage business start to tail off and we have a tightening of the economy. Here differentiated pricing ensures that both the borrower and lender benefit. The key is getting the right price both for the lender to be profitable based on their risk assessment involved and also represent a competitive and attractive price for borrowers.

Cotter, J., 2006, Recent Developments in the Irish Property Market. |

Professor John Cotter is director of the Centre for Financial Markets at University College Dublin School of Business. He is currently on sabbatical at the Anderson School, UCLA (john.cotter@anderson.ucla.edu). David Duffy (Economic and Social Research Institute), Annette Hughes (DKM Economic Consultants), Anthony O’Brien and Felix O’Regan (both Irish Bankers Federation) all contributed to this article.

|

| Article appeared in the November 2007 issue.

|

|

|