| No time to waste on implementing Solvency II |

Back |

| Solvency II is a vast document that requires a lot of insurers and reinsurers to implement. With a dealine for implementation of 2012, Samia Ahmed-Hossain argues that there is no time to waste if the legislation is to be fully implemented. |

Financial services organisations face yet another major challenge in the European Union’s new directive for insurers. Solvency II will have an unprecedented impact on the insurance and reinsurance ((re)insurance) sector. The proposed new EU legislation establishes a new framework to govern the capital requirements of insurance companies which has far-reaching consequences on how firms are managed.

In this paper we summarise the salient points of the Solvency II framework and examine some implications of Solvency II on the organisation, the processes and the systems.

What are the key principles of Solvency II?

Solvency II’s main objective is to protect the interests of policyholders and beneficiaries in the Union, through ensuring the financial stability of (re)insurance companies. The approach is to adopt regulatory capital requirements that are closely aligned to the risks in the business. The directive seeks to improve the competitiveness of EU insurers, both within the EU insurance market and internationally, by deepening the integration of the EU insurance market through a higher level of standardisation of the rules applied.

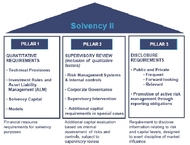

Drawing on the concept used for Basel II, Solvency II defines a mutually reinforcing three pillar structure which looks to ensure not only adequate financial resources, but also effective governance by firms, as well as increased market discipline.

In greater depth, Pillar 1 defines the financial resources that a company needs to hold in order to absorb major unforeseen losses. It uses a ‘total balance sheet approach’, considering both assets and liabilities. There are three levels in the proposed framework: technical provision, minimum capital requirement (MCR) and supervisory capital requirement. Technical provisions are a best estimate of the ‘exit value’ of the business (i.e., the amount a (re)insurance company would pay today if it transferred its business to another firm), plus a risk margin. The next level, MCR, is considered a level below which policyholders’ interests would be seriously jeopardised. Falling to this level would provoke immediate supervisory intervention. The required level is the solvency capital requirement (SCR) which will be calculated either using a ‘standard’ approach or internal models, subject to ‘use test’ and regulatory approval. The SCR calculation will include an evaluation of operational risk, along with insurance, investment and other financial risks.

Pillar 2 focuses on qualitative requirements which are seen as an essential complement to Pillar 1. The foundation for Pillar 2 is the requirement for insurance undertakings to have in place sound and effective strategies and processes to assess the risks to which they are exposed and to calculate and maintain appropriate capital against these risks, as well as associated reporting procedures. Firms will be required to undertake an annual self-assessment of these governance systems and their ongoing capital needs. This assessment feeds into the supervisory review process. If, as a result of the supervisory review, the supervisor concludes that governance systems are lacking, it may impose a capital add-on.

The final pillar, Pillar 3, seeks to enhance market discipline by the public disclosure of key information. The main provision is for reliable, consistent and understandable disclosure on a timely basis to maintain transparency and foster open information.

Full implementation of Solvency II is expected in 2012. However, many key details will be decided in the coming months. Insurers can benefit from the lessons learned from Basel II: an early start will provide greater options on ‘best-fit’ implementation and also optimise possibilities for strategic advantage alongside the transformation. Programmes of this nature take years and a mad dash to the finish line is best avoided.

What is the implication on the (re)insurers business?

One of the biggest impacts from Solvency II on insurance companies is the expectation for senior executives to demonstrate in-depth understanding of the framework, improved management of their capital and better decision-making as a result of their identification of key organisational risks. These requirements build a strong case for the implementation of a robust corporate governance structure. Good governance is about managing all the risks inherent in the business and addressing deficiencies, such as poor information flows, weak risk management process and procedures, as well as behaviour. The implementation of such a change demands active boardroom direction, a full understanding of the implications at all levels of the business, clear allocation of management responsibilities and the earliest possible investment of resources.

Companies can leverage value by integrating their corporate governance, risk management and regulatory compliance (GRC) activities thus increasing efficiency, consistency, and implementing legally sound structures. Solvency II creates a direct correlation between risk and capital, thereby providing an incentive for organisations to improve the quality of their risk management frameworks and systems in order to reduce the required regulatory capital. This provides a competitive advantage to financial services organisations with a strong GRC framework. For an individual organisation, the overall risk exposure will determine the capital requirement, and GRC initiatives are an important factor in reducing the amount of capital that needs to be held.

As previously indicated, Solvency II sets out the requirements for companies to establish systems, processes, and controls for effective risk management. For each company, regulators will assess the quality of the risk analysis and resulting capital evaluations against their own appraisal of the risk profile. They will also judge the effectiveness of the underlying reporting and governance procedures. Any cause for doubt or dissatisfaction may result in the application of an additional capital charge.

Solvency II sets out risk management and measurement objectives to ensure adoption of robust risk management processes that are carried out across the entire organisation and that form the basis for informing and directing the insurer’s decision making. To adequately meet these forthcoming requirements, insurers should explore the adoption of an enterprise risk management framework (ERM), including the addition of a chief risk officer or establishing an executive level risk committee or both. These management level governance structures should be supplemented by the creation of ERM teams where there is dedicated staff to focus on supporting ERM as opposed to having current staff sharing ERM responsibilities with their regular jobs.

The benefits of ERM are evident in the integrated view of risk management including consistent processes to analyse, evaluate and communicate risks. An ERM framework enables the implementation of strong controls and facilitates a strong risk culture and governance across the organisation.

Companies better able to manage risk will create the potential for significant competitive advantages, including:

- Holding capital costs money; therefore holding less capital will create a pricing competitive advantage

- Larger companies will have capital advantages through the presence of risk diversification within their larger - Small companies will be able to employ more focused risk management techniques in niche product areas

For ERM to be effective it must be embraced and owned from the CEO level and permeate throughout the organisation’s leadership. Some companies may need to plan for substantial changes in the strategy, operations and governance of their business. Starting early can not only cut the costs and help alleviate any last-minute panics; it also allows time to develop a dialogue with supervisors and embed the new risk and capital management framework into the strategic and operational management of the business.

In this respect, a key problem encountered by banks undertaking Basel II implementation was the lack of sufficiently skilled personnel to run risk management programmes and, where appropriate, their modelling systems to turn reams of analysis into usable information. Solvency II directive will require the establishment of the following functions:

- Risk management (and risk modelling where appropriate)

- Actuarial

- Internal audit

Internal control and compliance

The need for competent and suitably qualified resources is heightened by a ‘demand surge’ for personnel as the implementation deadline looms. Many institutions may find that suitable staff are unavailable or, if they can be secured, that pay and fees spiral inexorably upwards. Early recruitment activities and investment in staff training can ease implementation and help companies to embed the new regulations into ‘business as usual’, rather than relying on ad-hoc fixes or potentially expensive contractors.

The banks’ experience highlights the importance of securing input and support from all relevant departments as early as possible. In addition to asset and risk management, insurers are also likely to require input from underwriting, reinsurance and actuarial units. Good implementation means being willing and able to make organisation-wide changes – changes that reverberate from front office to board of directors, and from business units to IT. These transformation programmes will result in a substantial change to management initiative which will need to be commissioned, managed and controlled.

Another facet of Basel II implementation of particular relevance to insurers is the availability, or lack of, appropriate risk data for both management and modelling purposes. Information used for operating a financial institution is often entirely IT generated and controlled. This is especially applicable to insurers who rely heavily on historical data to underwrite their business and manage their risk exposures. There will be a greater emphasis on data with the introduction of the Solvency II framework which is heavily data-centric across all three pillars from the risk based capital modelling requirements for Pillar I, which is forecasted to require at least 10 years of historical data; to the Pillar II operational risk management across market risk, credit risk, life risk, health risk and non-life risk; and, further in the reporting requirements for Pillar III disclosure.

Technology is key, particularly in large complex organisations to collect, measure and monitor the data upon which risk management processes are built. Data will need to be captured and integrated from operational, transactional and financial sources. Complementary to the modelling efforts is the need for high quality data sourcing, cleaning and management. The Basel II experience suggests that it is prudent for insurers to take early action in investigating their company’s data availability and quality, not simply in theory but what is forthcoming in practice from business units. To fully undertake rigorous assessment and measurement of risks, insurers need to capture several years of quality data.

In addition to data systems, the insurance industry is forecasting significant investments in actuarial models, IT and risk management systems over a number of years. Before they can move forward, they need to understand operational and IT requirements - assess the infrastructure elements, applications and controls; investigate software tools to support the complex calculations for new reserve and capital requirements; review internal planning and controls for regulatory tracking and auditing and consider additional risk identification and mitigation strategies. Finally, explore developing synergies between requirements from Sarbanes-Oxley, IFRS and existing IT programmes.

When should (re)insurers act?

There is no excuse for inaction or delay. Given the enormous range of the Solvency II directive, a 2012 timeline appears extremely short. With appropriate planning, insurers can avoid the scramble and the associated costs faced by many banks in the implementation of Basel II. Experience suggests clear and tangible benefits for firms that take early action in developing models and data infrastructure, and building management buy-in and understanding both at the group level and across individual business units. These firms will be able to generate management insight and real capital and underwriting benefit - and will leverage Solvency II as a business opportunity rather than a compliance burden. |

Samia Ahmed-Hossain is a Manager in Advisory Services with PricewaterhouseCoopers.

|

| Article appeared in the October 2007 issue.

|

|

|