| Alternative energy investment grows with ecological concern |

Back |

| As fears about global warming and carbon emissions escalate, many investors are looking at the area of eco investment as an opportunity to make an ethically sound investment, but do they offer healthy returns? Jens Peers examines the investment opportunities that climate change is presenting. |

Among the more interesting aspects of the recent ‘Live Earth’ series of events across the globe was the fact that they were not followed by a welter of climate change denial on the airwaves. Quite the opposite, there was almost universal agreement that climate change is real. That it is being driven by mankind, and that it needs urgently to be addressed.

The scale of the challenge is enormous and will require major changes in the way we all live and do business in the future. It will also drive the development and introduction of new and innovative technologies in areas as diverse as energy production and water purification. This in turn is throwing up new investment opportunities.

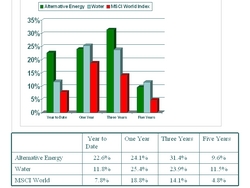

Of course, there is a negative side to all of this. One of the side effects of climate change is more severe weather conditions. This was most recently demonstrated by the devastating hurricanes of 2005 which almost destroyed New Orleans and a whole swathe of the South Eastern United States. | | Gross performance in Euro, to May 31st - Source KBCAM Ltd |

Naturally, insurance companies and property developers with an exposure to this region carry a much higher risk for the future. However, there are positives. And nowhere is this more amply demonstrated by General Electronic’s (GE) response to climate change and its implications. The world’s largest conglomerate has brought together all of its divisions and departments with any connection to climate change in a new group called Ecomagination.

This new reporting structure is intended to give a sharper focus to the company’s efforts in expanding sectors such as alternative energy. Indeed, GE is now the number one in the US in terms of installed wind energy capacity. It has achieved this position through a significant acquisition programme in recent years.

Another global giant with serious designs on the energy efficiency market is Philips. The Dutch company is gradually phasing out its production of incandescent lightbulbs and moving across to energy efficient CFL bulbs. Its intention is to swap its world leadership in the older type for the newer type. Based on the higher price points and higher margins which can be achieved for CFL bulbs, this environmentally enlightened strategy could also lead to increased profits.

Both of these are examples of how solid and well-grounded the so-called alternatives sector is. The main players are in fact the global leaders in mainstream sectors and the technologies are not necessarily all that new. Commercially viable wind power and CFL bulbs have both been with us for well over 20 years.

Of course, the key to major gains for investors still tend to lie in getting into an area as early as possible. However, this does not mean having to invest either in companies or technologies with no track record - far from it!

Take the example of Clipper Windpower - a company founded by the former management of one of America’s leading wind power players prior to it being taken over by Enron. This team is now back in the market with its new company which is bringing new wind generation technologies to the market. Within KBC’s Alternative Energy Fund, one of its active investment sectors is wind which has continued its strong momentum since the beginning of the year. One of the fund’s largest active positions is in Clipper Windpower which has gained 26 per cent in April of this year..

BP has recently purchased a major stake in the firm based on its very solid research and development pipeline. KBCAM participated in Clipper’s IPO at $1.90 and the company is now trading in and around the $9 mark.

Another interesting development at BP has seen the British oil company announce a joint venture with alternative energy specialist D1Oils in the UK. D1Oils specialises in the production of biofuels from a crop known as jatropha. This is a remarkable crop with a bright future in this area as it does not have any nutritional value and its use for biofuels will therefore not adversely impact world food markets. In addition, the crop will grow almost anywhere and will thrive in near desert conditions meaning that it will not impinge further on much needed arable land nor will it require the destruction of further tracts of rain forest for its growth.

Another interesting company that KBC has invested in is Nova Biofuels. This company produces biofuels from the waste by-products of abattoirs. Food safety issues such as BSE mean that many of the by-products which formerly made their way into the food chain in products such as jelly are deemed too risky. The use of this risk material for biofuel production is both environmentally responsible and potentially highly profitable for the producer as the raw material is effectively free.

But biofuels and wind are by no means the only energy sources which will play a major role in the future. There will be a balanced mix of energy, with oil, gas and coal continuing to play a role for the foreseeable future.

The role of the alternatives will continue to grow. Continuing advances in technology are making wind, biofuels and solar energy cost competitive with coal and gas for electricity generation and this trend will continue. It is for this reason that the largest investors in alternative energy production are the oil companies themselves.

Nuclear energy, on the other hand, does not hold out nearly as attractive a prospect as some would claim. The cost of building new plants both in financial and environmental terms is huge. The carbon emissions cost of the concrete element of a reactor is almost too enormous to contemplate and the 15 year planning to production cycle is so long that the financial investment would most definitely be better made in other technologies.

That is not to say that existing nuclear plants should not have their lifetimes prolonged through refurbishment. The concrete is already there and cannot be recycled in any way other than to have the life of the plant extended. This could be both financially sound and environmentally acceptable.

Solar, on the other hand, is an energy source which is already showing its worth both environmentally and in investment terms. The German solar industry is a case in point. From a near standing start not much more than a decade ago it is now a ?3 billion sector employing more than 40,000 people. It also boasts Q Cells, a German company which has recently become the world’s largest producer of solar cells.

Over that same period solar cells have become twice as efficient and have costs have dropped by some 30 to 50 per cent. Similarly, the cost of wind power has dropped by some 75 per cent over the past 15 years. There is no reason to believe that similar efficiency gains and cost savings will not be made over the next ten to 15 years making these technologies still more attractive.

With the strong political and economic focus on climate change and the requirement to tackle it, the future of investing in solutions to tackle climate change has never looked brighter. |

Jens Peers is head of Eco Strategies at KBC Asset Management.

|

| Article appeared in the August 2007 issue.

|

|

|