| Commodity bull run is coming to an end - but can gold escape the fall? |

Back |

| Despite concerns that the global commodity bull run is set to come to an end, Mark O’Byrne argues that gold is set to continue its period of growth and that reduced supply and increased demand will only help increase gold’s price. |

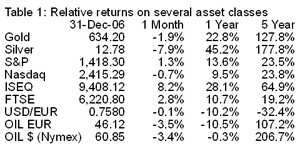

Gold returned 24.75 per cent in 2006, rising from $497 to $620 per ounce. It completed its 5th consecutive year of gains and is up by more than 140 per cent in the last 5 years.

It has thus outperformed all other asset classes in that period as can be seen in the performance table and chart. In 2007 it is up some 6 per cent to $657 per ounce and we believe it will surpass $700 by the end of 2007.

Gold Investments remains bullish on both gold, and particularly silver, and is confident that they are now both in multi-year bull markets. Commodities, like all asset classes, follow long term economic cycles. Commodities increased in value in the late 1960s and 1970s, broadly declined in value in the 1980s and 1990s to record lows and have been rising again since 2001.

We are not as confident on the outlook on some commodities such as base metals and some soft commodities, which are more cyclical in nature and would likely be affected by a slowdown in the global economy. Gold on the other hand is not solely a commodity but more importantly a universal currency held by every Central Bank of note in the world.

It is the only currency academically proven to have an inverse correlation to conventional assets such as bonds, equities and property. We believe gold will surpass its non-inflation adjusted high of $850 per ounce in 2007 and its inflation adjusted high of some $2,400 per ounce in the next 10 years.

These are not outlandish predictions, rather the majority of precious metal analysts in Wall Street and international banks are also bullish. Bloomberg has reported how a highly respected analyst, Louise Yamada sees gold surpassing $730 next year on its way to $3,000 within a decade. ‘Gold is the purest play against the dollar,’ said Yamada, managing director of Yamada Technical Research Advisors LLC in New York, former head of technical research at Citigroup. Yamada is highly respected and was was voted Wall Street’s best technical analyst from 2001 to 2004.

The Bloomberg article, ‘Gold Is Cheap, Yamada, Banks Assert as Sales Pared’, which quoted Yamada said that gold is becoming Wall Street’s darling again in 2007. Bloomberg’s Pham-Duy Nguyen said that this is due to ‘The swooning U.S. dollar, which has become a proxy for the slowing American economy and the nation’s humiliating lack of success arranging regime change in Iraq, banning weapons of mass destruction in North Korea and Iran, and reducing its trade and budget deficits.’

Yamada now has lots of company among the world’s biggest financial institutions. Deutsche Bank AG’s chief metals economist, Peter Richardson, made gold his favourite pick for 2007. JPMorgan Chase analysts John Normand and Jon Bergtheil on December 7th said only corn might rival gold as the best bet, while Merrill Lynch analyst Michael Jalonen elevated gold’s value through 2010.

‘If you can only make one commodity investment,’ gold is the ‘choice for 2007,’ said Richardson from his office in Melbourne.

The fundamental reasons for owning gold and silver in the last 5 years have not changed - indeed most of them have become stronger:

• Demand Factors

- Record and unprecedented US trade, budget & current account deficits

- Rising oil & energy prices

- Overvalued and plateauing property markets

- Rising interest rates in the US and globally

- Record consumer, mortgage and national debt levels in the US and much of the western world

- Increasing pensions difficulties with underfunded pensions and the ‘demographic time bomb’

- Growing realisation of the long-term impacts that global warming will have on all societies and economies as clearly outlined in the Stern Report

- Geopolitical instability and ‘The War on Terror’

- A depreciating and declining US dollar - the global reserve currency

- Increasing global investor demand for safe haven assets & Central Bank demand for gold in order to maintain full faith and provide stability to unstable currencies and monetary reserves

• Supply Factors

- It is estimated that all of the above ground stocks of gold could fit into a 20 meter high cube and is thus very finite

- Gold production is stagnating and gold output in the leading gold producing countries continues to fall year on year despite higher gold prices leading geologists to wonder whether we have reached the point of peak gold production

- It takes 10-15 years to take a mine to production

- High energy prices making mining an expensive proposition

- Environmental legislation stymies mine development

- Many mines are in unstable countries and regions such as South America, Africa, the Middle East and Russia

- Central Bank sales have slowed and in some cases reversed; the Russian and Chinese central banks are two of the more significant buyers of gold in recent months

Diversification of investments

Successful investing is about the diversification and management of risk. In layman’s terms this means not having all your eggs in one basket. We know from history that markets can crash and if you are not diversified your nest egg can be severely affected. This principle is an important one and should be observed by all investors - from ‘mom and pop’ investors to large institutions. From small savers whose primary asset is their Irish home to the National Pension Reserve Fund who have some 70 per cent of our national patrimony in equities, the vast majority of which are US denominated, and have very significant US dollar risk.

A healthy portfolio includes a wide range of assets including a variety of equities with exposures to different market sectors and regions; a variety of different countries’ bonds; a diversified residential and commercial property portfolio; a cash component and a 5-10 per cent allocation to gold bullion.

Holding precious metals in a portfolio can provide distinct benefits in the form of speculative gains, investment gains, hedging against macroeconomic and geopolitical risk and/or wealth preservation. Importantly, gold is the only asset class with an inverse correlation to the US dollar and to conventional assets such as bonds, stocks and property all of which are denominated in fiat currencies such as the US dollar, Sterling and the Euro.

Ibbotson Associates have shown in a June 2005 study, Portfolio Diversification with Gold, Silver and Platinum, how gold, and indeed precious metals, are the only one of the seven asset classes with a negative average correlation to the other asset classes. It is also worth noting that, excluding cash, precious metals are the only asset class with a positive correlation coefficient with inflation, which is further evidence that precious metals act as a hedge against inflation.

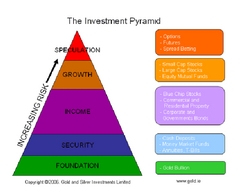

Traditional asset allocation theory, as represented by the investment pyramid (see chart 1), advocates higher risk speculations at the top, with lower risk assets at the bottom. Futures contracts, options, individual shares and spreadbetting should be placed at the top of the pyramid, while cash equivalents and fully allocated or taken delivery of physical bullion (as is done by the world’s Central Banks) should form the foundation or base.

Experienced and knowledgeable investors have long known that gold is a solid investment choice. Gold is stable in times of global geopolitical instability and when there is economic uncertainty, recessions and depressions. It is important that investors look at their portfolios holistically. Used correctly, gold and silver can be highly effective components of a properly diversified investment portfolio.

A strategic diversification into gold is merited in ALL portfolios, personal and institutional. A good rule of thumb would be a minimum allocation of some 10 per cent of gold.

Gold remains an under-appreciated, under-owned and under-valued asset. Most investors remain clueless about gold or at least fundamentally misunderstand it. At the beginning of the 1970s, when gold was about to undertake its historic move from $35 per ounce to $850 per ounce in the subsequent 10 years, the same observations would have been valid. The only difference between then and now is that the fundamentals are even stronger. |

Mark O’Byrne is the managing director of Gold and Silver Investments Limited.

|

| Article appeared in the August 2007 issue.

|

|

|