| Dealing with the continuing price volatility of oil |

Back |

Asset prices can be prone to large movements, and this year we have seen this in equity prices and commodity prices including oil. Recent volatility of around 2 per cent per day has led to uncertainty for treasurers and asset managers.

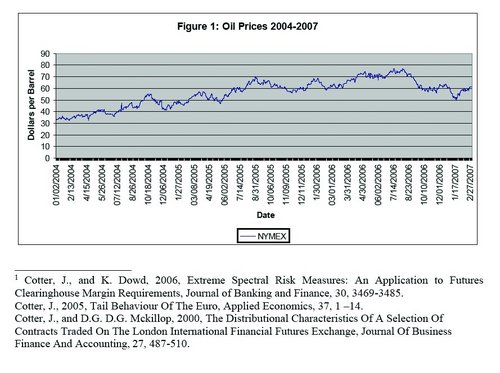

Most of this volatility has been on the upside with prices increasing dramatically over a short space of time (see figure 1). As we see here spot market oil prices (for immediate delivery) have approximately doubled in just two years before falling back from mid-2006.

Today the price of oil in spot markets in say six months time is uncertain although traders in futures contracts on NYMEX are currently forecasting that oil prices will fluctuate heavily and trend upwards.

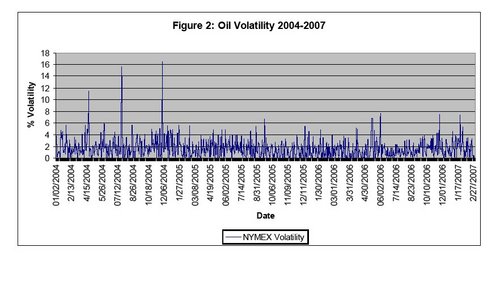

But will this happen? The short answer is we do not know. Pictures of past volatility (see figure 2) would certainly tend to agree with the former prediction with oil showing a propensity for very large movements since 2004. Moreover, the high levels of uncertainty associated with oil trading is set to continue given the turbulence from the main oil producing economies in the Middle East. The upshot is that we are very much in the dark about the price of oil in six months but prices will be volatile.

When oil prices surge as they have done we tend to spend a lot of time discussing alternative sources of energy. However, history suggests that it could take some time to remove our dependence. It is the number one used energy product and today it makes up almost 90 per cent of the fuel input in cars and aeroplanes. In fact, a recent forecast by Goldman Sachs has indicated that the peak production, and associated consumption, for oil is still ahead of us.

So businesses today face a very difficult dilemma of trying to substitute alternative energy sources while at the same time being heavily reliant on oil as a fundamental input into their everyday activity.

They know the former will take considerable time, so they have to look at strategies in dealing with the uncertainty currently associated with oil.

Current research undertaken in the Centre for Financial Markets at UCD may offer some respite in dealing with this uncertainty.2 Here, the role of futures contracts (with agreement today but delivery at some predefined date) are examined as to their potential for offsetting price risk, and in particular, oil price risk.3

Think of the following scenario: a business, say an airline, knows that they need oil at some future date, say six months hence. Lets say they require a volume that would currently cost ?10 million. The problem is that they do not know the price in six months. It could be ?9 million or ?11 million (or even higher - see figure 1).

A number of strategies are possible. For example a business could follow a no-hedge strategy where they take no action and hope that oil prices fall or remain constant. Alternatively the business could buy the oil today - a buy and hold strategy - and face the associated storage and financing costs.

Or it could follow a hedging strategy using futures or forward contracts to agree to buy the volume of oil in six months time at a set price that essentially would hedge against any price movements in oil over that period.

The price in the contract would be fixed today so the business would know with certainty what they have to pay when completing the transaction. So regardless of what happens to oil prices the business knows today, and with certainty, what they will have to pay.

The research suggests that this final strategy is the most promising. Calculations indicate that for the worst case scenario a substantial proportion (15 per cent) of the price risk is removed compared to a no-hedge strategy from an application to the world's most commonly traded commodity, the Nymex West Texas Light Sweet Crude contract. Moreover, the risk reduction gains are almost 60 per cent for the best case scenario.4

Now it must be recognised that there are trading costs (less than 5 per cent) with this strategy in using forwards or futures but these are negligible compared to the potential savings. The approach dominates the no-hedge strategy and avoids the extra storage and financing costs associated with a buy and hold strategy.

Thus hedging with forwards or futures where price movements in oil trading in the spot market are matched by those in the derivative is an important form of insurance against price uncertainty.

Predicting what is going to happen to the price of oil is a dangerous activity and given our dependence on this vital ingredient, it could also be very costly. Using futures or forwards gives a guaranteed price and eliminates the uncertainty for oil price movements in times ahead.

1Cotter, J., and K. Dowd, 2006, Extreme Spectral Risk Measures: An Application to Futures Clearinghouse Margin Requirements, Journal of Banking and Finance, 30, 3469-3485.

Cotter, J., 2005, Tail Behaviour Of The Euro, Applied Economics, 37, 1 -14.

Cotter, J., and D.G. D.G. Mckillop, 2000, The Distributional Characteristics Of A Selection Of Contracts Traded On The London International Financial Futures Exchange, Journal Of Business Finance And Accounting, 27, 487-510.

2Cotter, J. and J. Hanly, 2006, Re-evaluating Hedging Performance, Journal of Futures Markets, 26, 12-31.

Cotter, J. and J. Hanly, 2007, Futures Hedging Effectiveness under Conditions of Asymmetry, Working Paper WP-07-01, Centre for Financial Markets, UCD.

3Forward contracts organised on an Over-the-Counter basis with Banks would work in a similar way offering the same benefits as futures contracts traded on organised exchanges. The authors' use of futures is solely due to a price series being available for the completion of the analysis.

4Similar risk reduction possibilities are available for other assets such as equities, providing protection against the negative impact of unforeseen events.

|

John Cotter is a professor in the Centre for Financial Markets, School of Business, University College Dublin and Jim Hanly is a lecturer in accounting and finance at the Dublin Institute of Technology.

|

| Article appeared in the April 2007 issue.

|

|