|

|

Wednesday, 5th August 2026 |

| Convertible bonds rise to prominence |

Back |

| Convertible bonds are debt securities that can be converted into the common stock of the issuing firm at the option of the holder. With Euro-zone interest rates at a likely inflexion point, firms are likely to look more closely at convertible bond (CB) issuance to lock in low interest rates, pay down existing debt and increase leverage, write Bernard Murphy and Finbarr Murphy in this overview of the convertible bond market. |

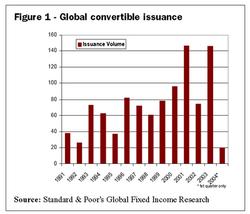

With Euro-zone interest rates at a likely inflexion point, firms are likely to look more closely at convertible bond (CB) issuance to lock in low interest rates, pay down existing debt and increase leverage. Approximately $80 billion of convertible bond debentures are issued each year and market intelligence suggests there is evidence of increasing secondary market activity within the hedge fund industry in Ireland. More generally, the low interest rate environment of the last decade has encouraged the development of a strong global market in CB issuance. Figure 1 shows the annual global convertible issuance since 1991. | | Figure 1 - Global convertible issuance |

Reflecting this developing interest in convertible debt, we provide a short educational article on convertible bonds, focusing on their basic properties and payoff characteristics. In a subsequent article we will demonstrate in greater detail how convertibles can be valued using the latest in ‘best-practice’ valuation algorithms and how they can be traded (and risk-managed) to implement for example, a sophisticated alternative investment strategy such as volatility trading.

Convertible trading

A convertible bond (CB) is a debt security that can be converted into the common stock of the issuing firm at the option of the holder. A CB therefore has a financial ‘structure’ which is part straight bond and part equity call option (or warrant). Which ‘component’ is the dominant determinant of value depends on prevailing conditions in both equity and bond markets at any given time and on the specific provisions which are attached to the CB contract. Some of these determinants of value are first defined and their effects then illustrated schematically in Figs. 3-5 following. First, a brief rationale is provided for convertible bond trading.

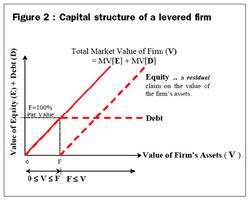

From the perspective of an institutional investor who purchases a convertible bond rather than the underlying stock, the premium typically payable1 over the current price of the stock can be intuitively justified on the grounds that the investor is limiting the downside risk of the investment to the floor level provided by the ‘straight bond’ component2. Although the CB investor does not receive dividends prior to conversion, his exposure to potential upside equity market movements remains the same as that enjoyed by a direct equity investor due to the conversion possibility. | | Figure 2 : Capital structure of a levered firm |

From the perspective of the corporate borrower, issuing convertible debt allows a company to source low interest3, subordinated debt which may be converted into new equity capital thus preserving existing cash reserves. Further advantages to the issuer include the availability of a source of funding when other markets are closed, a broad base of professional investors; as well as relatively well-established and liquid capital markets. The main drawback to an issuer is the dilution of existing shareholders on conversion.

From the perspective of the proprietary trader, convertible debt issuance is likely to be more common amongst relatively low investment grade - and hence probably more volatile – companies. For this reason, convertible (arbitrage) trading is increasingly being used by the hedge fund industry as a platform for implementing sophisticated volatility trading strategies4.

Finally, because CBs are more often than not subordinated debentures on low-investment grade companies, there is a significant exposure to credit risk (a combination of any or all of default risk, credit spread risk and downgrade risk) which along with interest-rate and re-financing risk needs to be taken into account in the valuation, trading and risk-management of these securities.

Valuation principles

In Figures 2, 3 and 4 we use ‘payoff diagrams’ to illustrate a number of valuation principles which must be taken into account in order to deliver an accurate estimate of value for a convertible bond.

First, Figure 2 illustrates the relationship between the market value (MV) of a firm’s assets and its capital structure – a mix of equity capital and risky debt.

The value of a straight bond at maturity for example can be expressed as Min[V,F] to reflect the credit risk faced by the debt-holders (i.e. the latter only get repaid in full at the maturity of a bond issue only if the value of the firm’s assets V exceeds the face-value amount owed F).

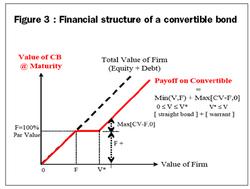

As an extension of Figure 2, the payoff characteristics of a convertible bond are illustrated by the ‘kinked’ value line in Figure 3. Using a technique known as financial ‘deconstruction’, the structure of the CB can be seen clearly as consisting of a straight bond and an over-the-counter call option on the equity of the issuing firm (i.e. a warrant). V denotes the ‘critical’ or optimal value of the firm at which conversion (into equity) will be optimal5. CV denotes the ‘Conversion Value’ - the ‘exchange-value’ of the bond when converted into (new) equity of the issuing firm. | | Figure 3 : Financial structure of a convertible bond |

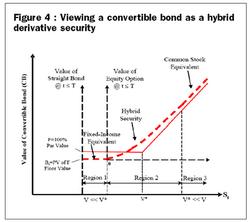

The dashed line in Fig. 4 following plots the value schedule for a CB on some arbitrary date ‘t’ which falls strictly before the first call date ‘T’ as explained below. Emphasising the derivative security properties of the CB, it is helpful to view the share price of the issuing firm (S_t ) as the ‘underlying’, although the pros and cons of conversion optimality can still be legitimately assessed from the perspective of firm value (V).

For example, in Region 1 if V << V then the equity-option component of the CB will be valued as a deep out-of-the-money (call) option and thus will have little or no value - the bulk of the convertible’s value will in fact be attributable to the straight bond component value B_t . The latter therefore can be thought of as providing a ‘floor’ level to the value of an investment in a CB security – but note that the floor level is not ‘guaranteed’, it can fluctuate up or down in response to stochastic interest rate movements (and indeed in response to movements in the credit-spread of the firm’s debt). In this region, the convertible security behaves very much like a straight bond – i.e. as a ‘fixed-income equivalent’ security.

In Region 2, if the current level of V is near V, the valuation of the CB will reflect non-zero contributions from a near-the-money equity option component _and_ a straight bond component. In this region, the CB displays part fixed-income like behaviour and part equity (or equity-option) like behaviour – in other words, a ‘hybrid’ security. Maintaining the approach illustrated in Figure 3, to emphasise the incremental contributions of both the fixed-income security and the equity-option components of market value, we overlay two value axes in the vertical plane. | | Figure 4 : Viewing a convertible bond as a hybrid derivative security |

In Region 3 if V >> V then the CB will be valued as a deep in-the-money call option on the ‘conversion value’ of the equity of the firm - the equity option component of the CB will completely dominate the straight bond component in value terms. In this region, the (non-callable) convertible security behaves as an equity security – any increase in the share price will be reflected in a proportionate increase in the value of the CB.

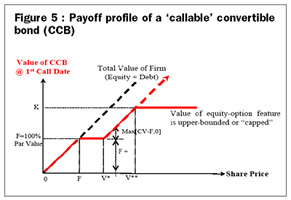

Finally, CBs are ‘callable’ at the discretion of the issuing firm – on the basis that it is desirable for the firm to retain the flexibility to re-finance its long-term debt should interest rates fall and / or the firm’s credit-worthiness improve at some stage in the future. However, the option to ‘call’ the debt is typically limited to a limited number of pre-determined fixed dates between issue and maturity and to pre-determined prices (collectively, the Call Price Schedule as defined in the CB Prospectus). For example, in Figure 5 the CB is callable on the first call date at a premium to face value (i.e. at K > F). This provision limits (or ‘caps’) the extent to which the CB (debt)holder could further gain from an increase in the market price of the firm’s equity above the corresponding firm value level V. For this reason, the value of a callable convertible bond at any time (CCB_t ) is less than that of the equivalent non-callable convertible (CB_t ).

From the perspective of a financial engineer,

CB_t = straight value + value of call option on stock

CCB_t = straight value + value of call option on stock – value of call option on bond.

A final point to consider in relation to the valuation of callable convertible debt is that the call feature is usually used by the firm to force conversion upon the convertible holder.

Summary

Equity price risk, interest rate risk, credit risk and re-financing risk are all ‘factors’ which influence the valuation (and hence the hedging) of an investment in a convertible debt security. Only the first two however might be properly considered as market (or traded) risk factors, although the expansion of the credit derivatives industry clearly provides the opportunity to hedge selected credit risk exposures. In a subsequent article we will overview a number of recursive valuation methods which can account for the aforementioned risk factors and contract provisions to give a robust estimate of convertible value. In the same article we will describe how CBs might be traded and risk-managed in practice to implement a convertible arbitrage trading strategy. | | Figure 5 : Payoff profile of a 'callable' convertible bond (CCB) |

1 The “conversion price” is calculated as the issue price of the convertible debt divided by the conversion ratio – the numbers of shares of common stock received‘ in exchange for a par-value ‘unit’ of convertible debt on conversion. The “premium” is defined as the positive difference between the conversion price and the prevailing share price at the time of issue.

2 Should the price of the common stock decline significantly (but as long as firm remains solvent and able to continue to service its debt), the price of the convertible bond will not fall below that of the straight bond “component”. Viewing the convertible as a “hybrid” security with a part straight bond and part warrant or equity-option structure, the value of the (deep OTM) equity-option component tends to zero under such a market outturn. These effects are illustrated in Fig. 4 following.

3 Low interest - since lower coupon income will be tolerated by investors because of the embedded equity option feature.

4 Hedge fund or “alternative investment” trading currently accounts for more than 70% of convertible trading volume in London and New York. Source : Financial Times, Weekly Review of the Investment Industry, April 11, 2005.

5 In terms of the underlying share price, V is reached when the prevailing share price equals the “conversion price” as defined in the CB prospectus at the time of issue.

6 Low interest - since lower coupon income will be tolerated by investors because of the embedded equity option feature. |

Dr. Bernard Murphy is a lecturer in derivatives and financial engineering on the MSc in Financial Services programme in the Kemmy Business School, University of Limerick, and Finbarr Murphy is a former convertible bond trader with Merrill Lynch and is currently working on a PhD in Finance in the Kemmy Business School, University of Limerick.

|

| Article appeared in the July 2005 issue.

|

|

|