| The risks from investing in convertible bond arbitrage |

Back |

| Convertible arbitrage strategy is pursued mainly by hedge funds and proprietary trading desks at investment banks, and is used to exploit inefficiencies in the pricing of convertible bonds by purchasing the undervalued security and hedging market risk using the underlying share. Although such strategies can lead to excellent returns, and in general market conditions there will be the benefit of added diversification, recent research has revealed that when equity markets become negative this benefit diminishes (perhaps when it is needed most), and in extremely positive equity markets returns may be poor due to the effect of falling implied volatility, say Mark Hutchinson and Liam Gallagher. |

New research being conducted jointly at Dublin City University Business School and University College Corki provides important findings for those considering an investment in convertible bond arbitrage. Evidence is documented showing that on days when equity market returns are extremely negative, convertible arbitrage exhibits negative returns. This negative return is due to increases in credit spreads. Evidence is also presented that on days with extremely positive equity market returns the returns from convertible bond arbitrage are also negative. This negative correlation is explained by the long volatility nature of convertible bond arbitrage. In extreme up markets implied volatility generally decreases having a negative effect o | | Table 1: Summary Statistics from January 1994 to December 2004 |

The convertible arbitrage strategy is pursued mainly by hedge funds and proprietary trading desks at investment banks. Arbitrageurs attempt to exploit inefficiencies in the pricing of convertible bonds by purchasing the undervalued security and hedging market risk using the underlying share. Arbitrageurs also often hedge credit risk using credit derivatives although evidence indicates that hedge funds following this strategy have significant credit risk exposure.

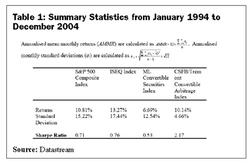

Risk adjusted returns from the strategy appear to have been excellent over the last ten years. Table 1 presents the average annualised monthly return, annualised monthly standard deviation and Sharpe ratio for the CSFB Tremont Index of convertible arbitrage hedge funds, the ISEQ Index, S&P 500 Index and the Merrill Lynch Convertible Securities Index from 1994 to 2004. The CSFB Tremont has the best Sharpe ratio, 2.17, by a considerable degree over this sample period. However it should be noted that the returns being analysed are for a hedge fund strategy index which may be overstated due to survivorship bias. n convertible bond arbitrage returns. | | European symbol - money |

Survivor bias exists where managers with poor track records exit an index, while managers with good records remain. If survivor bias is large, then the historical returns of an index that studies only survivors will overestimate historical returns. Also by looking just at return and standard deviation the full risk of the strategy may not be evident.

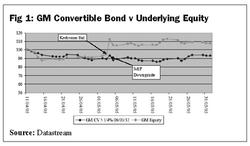

An example of the unanticipated risks has been the general widening in credit spreads in 2005. As a result those arbitrageurs who have not hedged credit risk have performed poorly. Reported returns to date in 2005 show the CSFB Tremont Convertible Arbitrage Index down 8.9 per cent. A good example of the difficulties faced by arbitrageurs this year is the General Motors trade. After a series of credit rating downgrades there was a market consensus that General Motors convertible bonds were undervalued. Many funds took long positions in General Motors convertible bonds and hedged with a short position in General Motors shares. On 4th May 2005 Kirk Kerkorian announced a tender offer for shares of General Motor’s pushing the stock up 18 per cent. On the following day Standard and Poor’s downgraded the credit rating of General Motors further to junk status. These two factors caused large losses for arbitrageurs as illustrated in figure 1 with the convertible bonds which arbitrageur’s were long falling in value and the stock which they were short rising significantly.

Anecdotal evidence therefore suggests that there may be considerable risks, beyond those captured in historical monthly hedge fund returns, from investing in convertible arbitrage. However are the events of 2005 a once off or is there more risk in this strategy than is captured by looking at returns relative to standard deviation using a measure such as the Sharpe ratio?

To answer this question the new research innovates by creating a simulated convertible arbitrage portfolio using historical date from 1990 to 2002. The study combines financial instruments into a portfolio in a manner akin to that ascribed to practitioners who operate the strategy. The portfolio is created by matching long positions in convertible bonds, with short positions in the issuer’s equity to create a delta neutral hedged convertible bond position which is rebalanced daily capturing income and volatility. Returns on each individual position are calculated daily as shown in Fig. 2. | | Fig 1: GM Convertible Bond v Underlying Equity |

Where is the return on position i at time t, is the convertible bond closing price at time t, is the underlying equity closing price at time t, is the coupon payable at time t, is the dividend payable at time t, is the delta neutral hedge ratio for position i at time t – 1 and is the interest on the short proceeds from the sale of the shares. Daily returns are then compounded to produce a position value index for each hedged convertible bond over the entire sample period. The delta neutral hedged positions are then combined into a convertible bond arbitrage portfolio. To confirm that the simulated portfolio has the characteristics of a convertible bond arbitrageur the returns of the convertible bond arbitrage portfolio and the returns from two indices of convertible arbitrage hedge funds are examined in a variety of market conditions. Results demonstrate strong positive correlations between the simulated portfolio and convertible arbitrage hedge fund returns indicating that the portfolio captures the characteristics of a convertible bond arbitrageur.

The study then goes on to test what effect adding a convertible bond arbitrage portfolio to a traditional buy and hold equity portfolio from 1990 to 2002 would have had. In normal market conditions the relationship between the two portfolios is very weak indicating the added diversification from investing in convertible bond arbitrage.  | | Fig 2: Returns on each individual position |

However, when the data is divided up according to equity market returns the results are striking. On days when equity markets are extremely weak (more than 2.5 standard deviations less than the mean daily return) the strength of the relationship between more than doubles. On days when equity markets are extremely positive (i.e. more than 2.5 standard deviations greater than the mean) the relationship becomes negative. For every 1 per cent increase in the long portfolio the simulated convertible bond arbitrage portfolio decrease in value by 0.25 per cent. This occurs on average four trading days per year over the sample period. This negative return can be attributed to the drop in volatility associated with extremely positive equity market returns.

These results suggest that for an investor considering adding convertible bond arbitrage to their portfolio when evaluating risk two things should be borne in mind. Although in general market conditions there will be the benefit of added diversification, when equity markets become negative this benefit diminishes (perhaps when it is needed most) and in extremely positive equity markets returns may be poor due to the effect of falling implied volatility. |

Mark Hutchinson is a lecturer in finance in University College Cork and Liam Gallagher is Professor of Finance at Dublin City University.

|

| Article appeared in the July 2005 issue.

|

|

|