| Irish pension funds shouldn’t be looking to diversify away from Irish equities - just yet |

Back |

| Despite the excellent performance of the Irish equity market over the past number of years, with allocation to Irish equities by managed funds standing at around 20 per cent, many funds have started to move out of Irish equities in order to lower the perceived risk profile. While in FINANCE February, Grainne Alexander of Mercer believed that this was a welcome development, this month Pramit Ghose takes a differing view, arguing that a holding now in Irish equities of around 21 per cent for a typical Irish pension fund is correct. He says the key principle to remember is that you cannot divorce market conditions from investment decisions and simply look at investment models in isolation and ignore the investment outlook for different ‘stock markets’. |

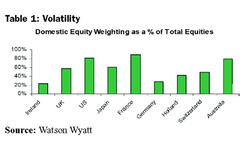

What is more important to investors - reward or the risk profile? For long term investors like Irish pension funds one would think that reward is the more important factor given that one can afford to wait for the reward to play out. However, in recent years it would appear that the risk profile argument has had the upper hand.  | | Table 1: Volatility |

This has manifested itself particularly in the unseemly rush by Irish pension funds out of Irish equities to lower the perceived risk profile. The arguments against the Irish equity market purveyed by investment consultants are well known and in fact have a good rationale. The worries relate to the small size of the stock market, the concentration in a small number of stocks, the concentration in very few sectors, and also a perception that volatility in the Irish stockmarket is higher because of the above factors, all of which have been heightened by Elan’s rollercoaster performance. However, if we look at the domestic weighting in equities of pension funds across the world we find that Ireland has one of the lowest such weightings.

Volatility

Taking this a stage further and working out pension funds’ concentration in the top ten equity holdings we see from Table 1 that for some of the more sophisticated pension fund markets such as the UK Holland and Australia, they have a higher concentration risk in the top ten holdings. So we can conclude initially that Irish pension funds are in fact more diversified against their international peers than you might think.

Top 10 equity holdings as a per cent of total fund

What are the important diversification principles? Is it simply to reduce risk? At Acuvest we think that diversification is worthwhile only if (a) it improves the portfolio’s return potential without increasing its risk profile or (b) it improves a portfolio’s risk profile without decreasing its return potential or (c) it does both of these. | | Table 2: Top ten equity holdings as a % of a total fund |

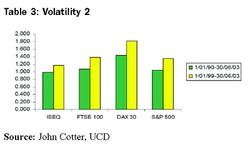

Lets look at some figures that have been compiled by Dr. John Cotter of the UCD Centre for Financial Markets. Obviously, we all know that Irish equities have performed well, but in fact you can see from Table 2 that Irish equities have, against the FTSE 100, DAX 30 and S&P 500 stockmarkets indices, demonstrated lower volatility and also lower correlation. These facts are initially surprising given the size of the market, but perhaps not when you think about it a little bit longer and you think how defensive the Irish stockmarket is.

Looking at Table 3 the correlation between the three stockmarkets shown, the FTSE 100, DAX 30 and S&P 500 is roughly 80 per cent, so the Irish market is actually much less correlated against these markets.

So the question pension funds have to ask themselves and their consultants is why is one switching to international equities which are highly correlated among themselves and moving away from Irish equities which have had a much lower correlation and lower volatility.

ISEQ correlation

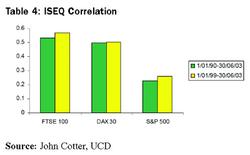

In my opinion the main reason for investing in Irish equities is to match the liabilities for Irish pension funds. The second important reason would be if the returns on offer from domestic equities appear to be superior than those on offer from foreign markets (see Table 4). In relation to matching liability growth, two main reasons emerge, first of all Irish equities are obviously in the domestic currency of the liabilities of the fund so there is no currency risk and secondly it is reasonable to assume that there is a strong link between salary growth, GDP growth and the domestic equity market returns. This is particularly relevant when the growth rate of an economy is markedly different from other economies, as we all know, that the historic growth rate in Ireland has been some where around 21⁄2 times that of the OECD since the year 2000. | | Table 3: Volatility 2 |

Economic growth rates

You have to ask yourself how could investments in international markets hope to match the salary growth associated with such strong Irish GDP growth which as we know was forecastable and known. This is not hindsight. No one is surprised by the fact that Irish equities have outperformed international equities with the growth rate that had been forecasted and the valuations of Irish stocks prevailing four or five years ago. Irish fund managers and stockbrokers are often accused of being biased towards the domestic equity market but in this particular case that doesn’t mean they were wrong! It was generally known that the valuations of Irish stocks versus their European and US peers was significantly cheaper and when you factor in the expected growth in the Irish economy it is not a surprise about the performance. Unfortunately this argument was rejected in favour of the risk reduction argument purveyed by investment consultants. And this is a very important principle that pension funds must not disregard; you cannot divorce market conditions and valuations from investment decisions and simply rely on models.

Looking to the future you can see that the forecast growth rates for Ireland, not unexpectedly, is significantly higher than the world economy outlook.

Economic growth forecasts

So if we were to keep our previous argument would it be logical simply to increase exposure to Irish equities? No is the answer, you still have to look at the valuations from the markets. Buying into something that has stronger growth doesn’t necessarily mean that it will outperform because you have to take into account how much of that future growth is priced in and when we look at the table below you see that Irish growth is starting to be priced in.

Price/earnings ratios

Historically when Irish price earnings ratios were the same or higher than the UK and Europe this tends to be when Ireland underperforms. Now of course we are not quite there yet and the growth rate in Ireland is expected to be very good, but perhaps it would appear that Ireland’s super normal growth rate is starting to be priced in to its stock market.

What is the appropriate Irish equity weighting?

If a Martian landed and was looking around at this problem he, she or it would probably say based on the strong performance, low volatility, and low correlation of the Irish stockmarket with other stockmarkets, matching benefits, and the growth outlook for the Irish economy, that 50 per cent of the total equity holding or 35 per cent of a typical Irish pension fund should be invested in Irish equities. Applying a practical hat, one has to adjust for the lower liquidity of the Irish stockmarket, a reasonable trustee expectation that the maximum individual holding in any one stock should not be more than 5 per cent, and the fact that the growth rate of the Irish economy is starting to be priced in. | | Table 4: ISEQ Correlation |

On that basis, a holding of some 30 per cent of the total equity weighting, or around about 21 per cent of a typical Irish pension fund, would probably be the correct weighting now. Interestingly enough, looking at the current mix of Irish managed pension funds we are not too far away from that at around 19 per cent. Looking forward in the expectation that the Irish equity market will continue to outperform other markets, and that over the next two or three years the valuations of Irish equities may in fact become higher than that of the European and UK stockmarkets, that will be the time to reduce the Irish equity rating perhaps down to 15 per cent to 20 per cent of the total equity holding or about 11 per cent to 12 per cent of a total balanced portfolio.

Conclusion

Irish pension funds’ search for diversification out of Irish equities over the past five or six years has unfortunately resulted in a cost in my estimation of around about €2.5 billion in terms of lost investment returns. In addition, pension fund portfolios instead of benefiting from diversification benefits have in fact experienced increased volatility and higher correlation. Finally, having spent a week in New York last November visiting about twenty top class US companies, the one abiding thought I brought home with me is that growth is scarce and that even the very best companies struggle to grow in this very competitive environment. But when we look at our own Irish equities, growth is easier to get and at a lesser valuation that international stocks. If there is one lesson to take from all this, it is again the principle that you cannot divorce market conditions from investment decisions and simply look at investment models in isolation and ignore the investment outlook for different stock markets. |

Pramit Ghose is head of investment strategy at Bloxham Stockbrokers and a founding director of Acuvest Investment Advisers. This article is based on a recent speech given by Pramit to the Irish Association of Pension Funds.

|

| Article appeared in the May 2005 issue.

|

|

|