| Sub-investment grade corporates should reduce their weighted average cost of capital through securitisation |

Back |

| New research shows that financial stress has increased dramatically for sub-investment grade companies across Europe, in contrast to A rated counterparts which have been hardly affected. Declan Lynch analyses the implications for European sub-investment grade companies. |

Despite increasing economic momentum across Europe, 2004 has been plagued with scepticism about the nature, depth and sustainability of the recovery. According to PricewaterhouseCoopers’ European Economic Outlook from June 2004, the Euroland economy is projected to grow by only around 1.5 per cent to the end of 2004, compared to 4.5 per cent in the US. A clear exception to this is the Irish economy, which has strongly outperformed average European growth levels for several years.

| | Declan Lynch is executive vice president of Demica. |

In October 2004, the Bank of Ireland’s chief economist Dan McLaughlin stated that he believed Ireland’s economic growth has the potential to reach 6.5 per cent a year. However, economic optimism on this scale masks the reality that the picture is not so rosy across the board. Despite the soaring profits generated by highly-rated corporates, the sub-investment grade community is labouring under a crippling debt burden that threatens to jeopardise Ireland’s economic growth potential.

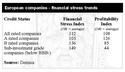

| | European companies - financial stress trends |

Furthermore, equity finance all but disappeared in the early years of the new millennium, and European companies were forced to raise considerable levels of debt finance (in some cases rapidly followed by dwindling expectations of a trading return to finance that debt). Consequently, there is considerable suspicion that the burden of servicing this debt legacy is continuing to suppress profitability and growth. Corporate financing has come under the spotlight as companies seek to improve liquidity, reduce the debt burden and support recent tentative growth.

The depressed capital markets value of many organisations, compared to the heyday of around the new millennium, has led to yet another phenomenon - an upsurge of interest in MBOs and LBOs across Europe. It is the aggregated view of various research bodies that around €150 billion (in equity) of LBOs will have been concluded in Western Europe between 2003 and 2005. The cost of debt is expensive as companies that have been subject to an LBO often have their credit rating downgraded to sub-investment grade status precisely because of their leverage.

The rise of securitisation

The combination of debt legacy and increased LBO activity is leading an increasing proportion of financial managers to explore alternative, less costly lines of working capital finance. Securitisation of corporate assets, which enables better-rated asset-backed finance to be raised from the capital markets, has come onto the radar of most financial managers. Demica research earlier this year revealed that trade receivables are the most popular asset to securitise, that invoice securitisation is expected to accelerate towards 2005. The reduction in costs are considerable, as when security such as invoice debt can be put behind the borrowing, interest costs are often reduced to just 50-100 points over Euribor. One recent transaction saw a blue chip European corporate execute a transaction which saves over €5 million per annum in interest costs. This involves securitising invoices from various operating companies, and over the term of the AAA-rated deal, the net present value saving is €30 million. The originating group is rated BB-.

Furthermore, many private equity houses are turning to invoice securitisation as a means to free up development capital as soon as possible after conclusion of the LBO. Their interest in this financing tool has less to do with reducing overall interest costs, and more to do with releasing working capital to invest in marketing, product development, channel development, sales incentives, and other catalyst to market growth. This allows them to grow the acquired company more rapidly, reduce the period it takes to divest it and realise the return on investment for investors. Furthermore, the typical length of an invoice securitisation deal of 5-7 years is a very good fit with the exit strategy of many private equity houses.

The trends in financial stress

In the light of all these factors, Demica commissioned research into the current state of financial stress amongst non-financial European companies in various rating bands. The study measured financial pressure in a model centred mainly, but not exclusively, around interest cover (the relationship between profits on the one hand, and interest payments on debt commitments on the other). The most recently reported year of results were compared to the previous year in order to see whether financial stress had increased or decreased.

Change in financial stress was measured for European companies in different credit rating classes, amalgamating the main global credit rating companies systems into: A rated companies; B rated companies; and sub-investment grade.

The picture that emerges from the research depicts a scenario of polarisation. Financial stress has increased for all rated companies in Europe. However, the increase has been absolutely marginal for A rated companies (3 per cent), substantial for B rated companies (36 per cent), and punishing for sub-investment grade companies (49 per cent)1. The sound appear to be getting sounder, but the highly indebted, with some notable exceptions, are in danger of becoming terminal.

This research emphasises the importance and urgency for sub-investment grade companies across Europe to at the very least to reduce their weighted average cost of capital through lower cost alternative finance such as securitistation. This also has an economic importance, in that further company failure, or just severe difficulty, could dent the confidence of the current recovery, certainly in continental Europe, and could even slow down progress in strong economies such as the UK.

Conclusion

The Demica report revealed that the gradual overall economic progress in Europe, and stronger growth rates in economies such as Ireland, is hiding the fact that financial stress is increasing amongst more indebted companies. The cost of servicing current debt commitments is becoming more of a burden, and trading improvements have not been sufficient to halt the increase in financial stress amongst B-rated companies as a whole, and sub-investment grade companies in particular. It is therefore imperative for these highly stressed companies to seek alternative, lower-cost financing options. Previous Demica research unveiled a growing enthusiasm amongst European corporates for invoice securitisation, with motivations ranging from sheer debt burden to realising value from LBOs. We predict that several high-profile invoice securitisation transactions will emerge from the corporate sector over the next few months.

Key findings

• Across Europe, sub-investment grade companies are coming under increasing financial stress, despite the general economic recovery.

• For these highly stressed companies, profitability has fallen dramatically, while debt burdens have not been substantially reduced.

• In contrast, financial stress amongst A rated companies has stabilised and profitability is rising.

• Sub-investment grade companies, in particular, are caught in an expensive debt cycle, and are eagerly seeking ways of reducing their interest costs through asset-backed financing alternatives such as invoice securitisation and other means.

• Post LBO companies are another community under financial pressure, and are eagerly turning to invoice securitisation to free up working capital and realise their ROI.

1 Rating classes follow Standard and Poor’s terminology ; sub-investment grade defined as companies with a rating below BBB- |

Declan Lynch is executive vice president of Demica.

|

| Article appeared in the May 2005 issue.

|

|

|