| IAIM member survey: retail assets rise by 17 per cent in 2004 to €22 bn |

Back |

| Retail assets of Irish Association of Investment Managers (IAIM) members rose by 17 per cent in 2004 to reach €22 billion, boosted by the contribution from Special Savings Investment Accounts (SSIAs) at €560 million, writes Gary Connolly. |

The eighth annual survey of investment trends in the Irish retail funds market was published by the Irish Association of Investment Managers (IAIM) in March. Total assets under management by  | | Gary Connolly - Investment Development Manager, Setanta Asset Management Limited |

IAIM members on behalf of domestic and international clients amounted to €200 billion at the end of December 2004. Retail assets of IAIM members rose 17 per cent in 2004 to €22 billion. Net cash flow into retail products in 2004 was just under €1.9 billion. This represented a modest five per cent decline on 2003, but still well ahead of 2002. The make-up of retail fund flows has changed considerably in the past 2-3 years. Two years ago net flows into with profits accounted for over half of the total flows in to all retail products. In 2004 the net flow figure into this category turned negative (albeit only marginally) for the first time.

Despite the lapse in with-profit flows IAIM members have been successful in plugging the gap and increasing net fund flows by over a quarter since 2002. Clearly, the contribution to fund flows from SSIAs, at €560 million, in 2004 has helped shore the gap. Notwithstanding the fact that 80 per cent of SSIA holders opted for deposit based products (which are not captured in this survey), the 20 per cent that chose equity based products still represent a significant proportion - 30 per cent - of retail fund flows. The intrepid have been rewarded, as the average managed fund cost average gain since May 2001 is 9.3 per cent (to the end of December ’04). This compares to a c. 7.5 per cent gain on a deposit earning a fixed 4 per cent p.a. return*. The comparison with the majority of SSIAs that started towards the end of the period, May 2002, is even better from an equity perspective, as investors would have missed out on the worst of the bear market during this period.

| | Table 1: Retail assets of Irish Investment Industry |

It is worth recalling that SSIAs were launched shortly after the end of the equity bull market; a period during which investor confidence in capital markets was severely undermined. The uncovering of major accounting and governance scandals rocked investor confidence. Warren Buffet’s comment at the time, ‘There is seldom just one cockroach in the kitchen’, proved prescient as scandal after scandal was unearthed. Against this background it is not surprising that many chose the safety of deposit based products.

Equity markets have run fairly strongly in the last two years, but in many cases only unwinding some of the damage inflicted during the previous three years. That said, the ‘wall of worry’ that stockmarket investors are climbing has become less steep. As always, the challenge for the IAIM is to adapt to changing investor demands. Probably even more so than last year, the current focus of investor demand is property related.

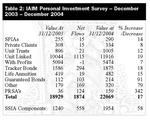

Appetite appears borderless with hotel conference facilities bursting at the seams with property exhibitions on destinations from the Canadian Rockies to Christchurch New Zealand. Kuwait has even found its way onto the radar of Irish property investors. The high-stool dot com discussions of five years ago have morphed into debates about the best value exotic property destinations. The value in property almost anywhere outside Ireland is apparent. The ability to buy a summer retreat  | | Table 2: IAIM Personal Investment Survey – December 2003 – December 2004 |

in Turkey for less than the price of a car park in Dublin city admittedly has its attractions. The dot com discussions of five years ago came to an abrupt end. What the high-stool debates will be in five years time is anyone’s guess, but lets hope it has a happier ending.

There is no suggestion that investment in property is misguided, however diversification should always be uppermost in investors minds when evaluating investment options. There were many scalded by the technology crash five years ago but for those that were adequately diversified the pain was limited.

Alongside the results of the survey the IAIM made a submission to the Minister for Finance on a new savings incentive scheme designed to replace SSIAs and to encourage continued long term savings. Having persuaded very large numbers of savers (in many cases first time savers), to enter into multi-year savings arrangements, it would be unwise to allow the savings habit to fall away. This is against a background of a recognised problem of inadequate retirement provision and a propensity for ever increasing personal indebtedness. The proposed product, called a Flexi Investment Account, is aimed primarily at those on low incomes. The scheme involves utilisation of existing tax allowances for pension fund contributions and offers access every five years to 30 per cent of the previous five years investment. All proceeds of an FIA would be tax-free at retirement. This proposal is not based on a ‘give-away’ product but one which continues to promote long-term saving (by using existing tax incentives) and similar to SSIAs should be available in either deposit or equity form.

The Government will undoubtedly receive several submissions from interested parties in the coming months. Time is certainly on its side with the first maturities from SSIAs over a year away. Whatever the intentions are for the estimated €14 billion maturing (according to Goodbody Research) in 2005/06, the regular savings momentum should not be allowed to wane.

*Based on even contributions from May 2001 to December 2004 a deposit account paying 4 per cent interest is worth 7.5 per cent more than the sum of contributions. |

Gary Connolly is investment development manager at Setanta Asset Management,and is chairman of the IAIM’s retail committee.

|

| Article appeared in the April 2005 issue.

|

|

|