| Alternative Investments - can fine wine continue to out-perform ? |

Back |

| Fine wine is attracting growing interest as an alternative investment thanks to disillusionment with traditional asset classes such as equities, writes James Miles, and some headline grabbing vintages from the world’s leading wine regions in recent years, particularly Bordeaux 2000 and 2003. |

Indeed, while wines from Burgundy, Rhone, Italy, Champagne and areas of the New World do provide opportunities to make money, Bordeaux - due to greater liquidity - remains the blue chip region and attracts the lion’s share of speculators interest.

The investment case for fine wine is compelling due to growing demand, finite supply and tax efficiencies (i.e. for occasional traders, profits on wine sales are not subject to capital gains). These strong fundamentals have led to some pretty spectacular profits in the past. For example, if you were lucky enough to purchase a case of Chateau Petrus 1982 on release in the spring of 1983 for ?450, you would now be sitting on a gain of about 3,200 per cent. The current resale value is approximately ?15,000!

Indeed, demand for wine at all levels has enjoyed strong growth in the last two decades due to increasing consumption and changing tastes in non-wine growing regions (such as UK, Ireland and Asia). The independent writings of all-powerful wine critics like the American Robert Parker - have fuelled this growing thirst for the top wines by helping the consumer to separate the wheat from the chaff with their tasting notes and scores having a huge impact on prices. | | Table 1: Liv-ex Claret Chip Index Rel to FTSE 100 |

At the same time, strict classification rules - particularly in France - make increasing production of the finest wines very difficult. Furthermore, wine is not differentiated simply by Chateau but also by vintage and there can be a big difference in the quality of the wine from one vintage to the next. When a bottle of Chateau Lafite Rothschild 1982, for example, gets drunk, unlike a bag of sugar or a tonne of copper, it is not easily substituted. In this way, wine from the best estates and vintages appreciates as available stocks are consumed.

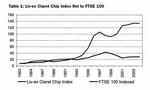

Indeed, when investing in wine, there is a strong argument for simply buying the best. This is illustrated by the Liv-ex Claret Chip Index above, which has outperformed the FTSE 100 by a considerable margin over the last 20 years. The ‘Claret Chip’ contains just 33 wines made up of ‘First-Growths’ (i.e. Chateau Haut Brion, Lafite Rothschild, Latour, Margaux and Mouton Rothschild) since 1982 that get a score of 95 points or more from Robert Parker. In other words, these are the cr?me de la cr?me of the Bordeaux market. | | Table 2: Top Claret Vintage POPs Relative to Fair Value |

Investing in fine wine, however, is not without risks! Picking the right wines and vintages is crucial. The 1997 vintage, for example, was a disaster for speculators. Released on the back of two successful campaigns (in 1995 and 1996) and in the early stages of the Asian crisis, buyers at opening prices have seen losses of up to 50 per cent. It is also important that wines are purchased ‘in bond’ to avoid paying duty and VAT, and that wines are well cellared, because the condition and provenance of the wines will affect the sale value. Above all, however, it is essential that when buying and selling fine wine, you have a good idea of what the market price is. The internet (and price tracking services such as our own) has improved transparency dramatically, but there can still be large discrepancies between merchants’ prices. | | Table 3: Claret Vintages Rel to Fair Value |

The market for top Bordeaux wines in recent years has been characterised by two very successful but somewhat over hyped vintages 2000 and 2003. Indeed, Robert Parker, described 2000 as ‘the greatest vintage ever’, which drove prices to unprecedented levels. This trend was repeated in 2003, a vintage that also produced some excellent wines, but it has left young wines looking expensive against the best wines from older vintages. Some of the most ludicrous examples, being Mouton Rothschild 1986 (a 100 point wine) which trades at roughly ?2600 against the 2000 (a 97 point wine) at ?2400, despite a higher score and an additional 14 years of bottle age. Sillier still is Lafite Rothschild 1996 & 2000 (both 100 point wines), which trade at ?1900 and ?2600 respectively.

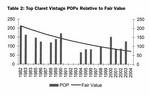

Nobody disagrees that some great wine was made in 2000 & 2003, but the reality is that the demand supply equation does not start to get attractive with Bordeaux until they are ready for drinking and young 2000s or 2003s are not going to be ready for 10-20 years. That represents an awful lot of opportunity (and storage) cost. Indeed, inevitably if one is going to finance the cost of holding claret for 10 or 20 years one requires a substantial discount to mature stock to justify the wait. As the chart shows below, this is simply not reflected in the market at the moment.

The chart above shows the average POP ratio (our loose measure of value which divides the price by Parker points to ascertain what one is paying per point) for the top 15 clarets in all of the decent vintages of the last 20 odd years. Indeed, 2000 is more expensive on this measure than any vintage except 1982 and 1990 and 2003 is even more expensive than the highly rated 1986. The blue line in the chart attempts to plot fair value by taking the average POP of all the back vintages and discounting them by the 10 year Gilt yield to reflect the opportunity cost of holding the wines.

As the chart above shows, this makes the great vintages of recent years look grossly over priced relative to the back vintages. So either new vintages are a sell or the best wines from 1982, 1986, 1995 and 1996 represent fantastic value at current levels. |

James Miles is a director of Liv-ex Ltd (the London International Vintners Exchange) and a former equities broker with BNP Paribas. Liv-ex is an independent trading and settlement platform for the fine wine trade. Liv-ex also sells price and other market information to private collectors from www.liv-ex.com.

|

| Article appeared in the October 2004 issue.

|

|