| Accountancy firms’ fee income growth eases, but IFRS boost expected |

Back |

| Ireland’s main accountancy firms notched up impressive gains in business during 2004, with overall fee income up 10.9 per cent at €636.4 million. However, in light of the accelerating pace of the economic recovery, growth was perhaps not as robust as expected, coming in under the 15 per cent level recorded last year. But while an improving economy and upbeat projections for next year point to expectations of healthy industry potential going forward, most firms have identified the implementation of IFRS in 2005, as among the most significant factors likely to affect business, with 16 of the 17 surveyed by FINANCE predicting an increase in fee income arising from the new rules. |

As predicted last year, KPMG pipped PricewaterhouseCoopers’ (PwC) to the top spot as Ireland’s largest accountancy firm in terms of fee income – but only just. Last year PwC came in first with just €1m extra fee income than KPMG, but this year it was KPMG’s turn to take top spot – and by the same margin. Fee income at KPMG was €152 million, an increase of 12.6 per cent on the year. At PwC, fee income was up 11.0 per cent on last year at €151 million. However, PwC will be encouraged by the margin of growth, which was significantly ahead of last year’s expansion of just 4.6 per cent. KPMG’s activities also benefited from the first full year inclusion of the activities of Andersen, which it acquired in 2002. (see table 1) | | Table 1: Fee income (€ million) |

Profitability

As per last year, the figures show that KPMG and PwC remain almost deadlocked in terms of fee income and market share. Both have cornered almost 24 per cent of the accountancy market, with KPMG just shading its main rival at 23.9 per cent, compared to a 23.7 per cent share for PricewaterhouseCoopers.

For KPMG, this represents a very small increase in its market share, as in 2003 is share was 23.5 per cent. PwC has maintained the same level of market share it had in 2003, at 23.7 per cent, failing to regain the level of market share it had in 2002, at 27 per cent, before the sale of its consultancy arm, PwC Consulting.

Elsewhere among the ‘Big 4’, Ernst & Young notched up fee income of €93 million, up just 5.68 per cent from €88 million last year, with a market share of 14.6 per cent compared to 15.3 per cent previously. And finally, Deloitte had income of €87 million, a substantial increase of 16 per cent from 2003. | | Table 2: The efficiency factor - income per staff member 2004 (€ 000) |

As the figures show, the hold of the Big 4 companies on the accountancy market remains seemingly unassailable, with a further significant increase in market share won this year. KPMG and PwC between them control almost half of the market, and when Ernst & Young and Deloitte are taken into account, the portion of the market cornered rises to 75.9 per cent. This compares to 75.6 per cent last year.

While there is little likelihood of any mergers among the Big 4, the increasingly competitive market is expected to lead to more consolidation among smaller firms. Middleweight firms such as BDO Simpson Xavier, which has already snapped up at least one firm over the past year, and smaller operations such as Grant Thornton and Mazars are all possible merger makers. | | Table 3: Staff numbers |

Beyond the Big 4, the Irish accountancy industry has put in another fine year, with most of the other 13 firms surveyed by FINANCE notching up moderate to impressive annual gains. Leading the best of the rest is BDO Simpson Xavier, which is well ensconced in the number five position, and well ahead of its nearest rival, Grant Thornton. BDO’s total fee income came in at €51 million, an increase of 14.3 per cent on the previous year. However, its market share fell slightly to 8.0 per cent from 8.4 per cent in 2003.

Grant Thornton, with fee income of €20 million, up a strong 14.3 per cent on the year, saw its market share rise slightly to 3.1 per cent from 3 per cent.

Seventh in terms of size is Mazars, with fee income of €14 million, up 11.1 per cent and carving out a market share of 2.2 per cent. Next is Farrell Grant Sparks, the third fastest growing Irish accountancy firm in 2003, with fee income up 17.7 per cent at €12.6 million. | | Table 4: Recruitment |

However, the two best performing firms are significantly smaller than their more well known peers. Nonetheless, Caplin Meehan, the smallest firm surveyed, saw its fee income jump 19.7 per cent to €3.6 million over the past year.

The next best performer was Horwath Bastow Charleton, with growth of 19.6 per cent and income of €8.4 million. The only firm to record a decline in income for the period was OSK, which saw fees generated fall 3.7 per cent to €5.3 million.

The survey clearly shows a significant disparity in performance between the smaller accountancy firms, with annual growth at the ‘Big 4’ firms at 11.3 per cent, suggesting that while some have been able to grow their businesses extremely successfully, others are finding growth opportunities rarer; perhaps an indication of future consolidation opportunities within the sector as more aggressively expanding firms squeeze out their weaker peers. | | Table 5: Recruitment trends |

The ‘efficiency’ factor

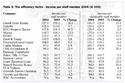

This year, for the first time, we have calculated the ‘efficiency’ of each firm, by calculating not only the income per partner generated, but also the income per staff member (see table 2 and 3). Based on this calculation, Farrell Grant Sparks has emerged as the most ‘efficient’ firm, with its 99 staff members generating income of €127,273 each, followed by Deloitte, with income of €118,326 for each of its 738 staff members, and BDO Simpson Xavier, with €117,771 for each of its 433 staff members.

When just the chargeable staff are examined, Farrell Grant Sparks remains in the lead, with income of €140,000 for its 90 chargeable staff, but this time is followed by KPMG, with income of €136,079 for its 1117 chargeable staff, and Ernst & Young, with income of €135,568 for its 686 staff.

In terms of fee income per partner, both KPMG and PwC reversed last year’s declines. KPMG’s 62 partners generated an average income of €2.5 million each, up 16.2 per cent on the year. Similarly impressive was PwC’s performance, where its 70 partners won annual fees of €2.2 million each on average. This marks an increase of 11 per cent on 2003 and a significant turnaround from that year’s decline in productivity of 3.47 per cent on 2002.  | | Table 6: Areas of strongest growth by company |

As was evident last year, the gap between the fee income per partner at the ‘Big 2’ and the other two members of the ‘Big 4’ is narrowing significantly. Deloitte’s 41 partners are snapping at the heels of their larger peers, with an average fee income of €2.1 million, up 10.3 per cent on the year. Ernst & Young, however, was among a number of firms that saw fee income per partner down on the year. Each of the company’s 50 partners generated an average of €1.86 million, down 2.8 per cent on the year. However, some of this can be attributed to the increase in partners from 46 in 2003.

BDO, Farrell Grant Sparks and HLB Nathans all saw an average of over €1 million per head. BDO’s 44 partners generated an average €1.2 million, an increase of 15 per cent. Farrell Grant Sparks’ 12 partners won business averaging €1.1 million per head – up 17.8 per cent, while HLB’s seven partners saw their productivity rise 14.4 per cent to €1 million. With an increase in partners at both Mazars and Russell Brennan Keane, average income per partners slid downwards at both firms.

Recruitment

The impressive growth in fee income among the country’s main accountancy firms was achieved against a backdrop of surprisingly significant staffing changes (see table 4 and 5). Although, overall, total employment among the 17 firms was almost unchanged at 5,814 (+ IFAC which did not disclose its staff members), some firms grew business with more staff, while others actually generated more income on fewer staff. The number of partners, however, grew slightly faster than overall staffing levels, rising 3.6 per cent to 372. PwC increased its staff numbers by 1.7 per cent to 1,440, while its closest rival, KPMG, cut staff by 4.2 per cent to 1,357. Ernst & Young increased its staff by 4 per cent to 842. Deloitte was among the fastest growing firms in terms of payroll, with staff numbers up 11.8 per cent to 738.

Elsewhere, Horwath Bastow Charleton, which was among the top performers in growing its fee income, hiked its staff by over 18 per cent to 110. As already mentioned, a number of companies cut staff, with OSK topping the axe list with over 22 per cent of staff shed, culling its payroll from 68 to 53. Also wielding the axe was BDO Simpson Xavier, where staff levels were cut by 9.4 per cent to 433. Few firms shed partners, although KPMG dropped two, leaving 62 and BDO cut its compliment of partners by four to 44. Ernst & Young added four partners during the year, bringing its total to 50, while PwC was unchanged at 70. Grant Thornton added three to its partner tally, bringing it to 22. | | Areas of strongest growth by sector |

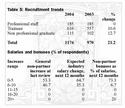

Recruitment in the industry is expected to be up by 21 per cent on last year, according to responses to the survey, with 1176 additional staff members set to be recruited between June 2004 and June 2005, compared to the 970 recruited for the same period last year. This breaks down into an additional 616 trainees, 115 non professional graduates, and 185 professional staff.

When looked at by company, PwC leads the pack, with some 150 professional staff expected to be taken on between June 2004 and June 2005 compared to just 60 between June 2003 and 2004. PwC also plans to take on some 195 trainees. KPMG intends to grow its professional staff by 40 by June 2005, with 170 trainees expected to be recruited. Ernst & Young has pencilled in recruitment of 31 professionals and 91 trainees, while Deloitte sees itself taking on 50 professionals, 30 non-professionals and 100 trainees. Among the smaller firms, BDO will take on 23 professionals and 39 trainees, while Grant Thornton will take on 14 professionals and 20 trainees.

Salaries

Although recruitment is up on last year, salaries are not. At the last non-partner general review, 53 per cent of employees received an increase in the 0-5 per cent range, compared to 47 per cent last year, while 47 per cent got an increase of between 6-10 per cent, compared to 53 per cent last year (see table 5). As was the case last year, there were no increases of above 10 per cent.

With regard to the coming year, the majority of salary increases will be in the 0-5 per cent range (65 per cent), with just 35 per cent getting an increase of between 6-10 per cent. As was the case last year, most of the bonuses granted will be in the 0-5 per cent of the overall salary figure (73 per cent), with 7 per cent in the 6-10 per cent range. Up on the past two years however, is the number who will receive a bonus in the 20 per cent plus range – 20 per cent. Employees at BDO Simpson Xavier are set to do the best, with bonuses expected to be around 30 per cent.

Growth areas

Amongst the contributing firms, 31 per cent voted corporate finance (up from 24 in 2003) as being the biggest growth area over the past year, followed by tax at 25 per cent (up from 24 in 2003) and management consulting at 19 per cent (up from 12 in 2003) (see table 6). The growth in corporate finance is indicative of a wider trend in the overall market, as improving economic conditions are resulting in corporates returning to the corporate finance market. Indeed 2004 saw the first IPOs since 2000, with both eircom and C&C floating on the Dublin and London markets. Moreover, merger and acquisition activity has also been at a high level over the past year. |

|

| Article appeared in the October 2004 issue.

|

|