| National Debt falls below 50% of GNP |

|

| |

As mid 2026 approached, the economists at the Department of Finance running their simulations ahead of the ‘National Economic Dialogue’, held on June 15th, will have been encouraged by latest debt statistics from the NTMA, and other indicators, such as the May Exchequer returns to adopt perhaps a braver advisory stance this year regarding tax reliefs for the long suffering Irish taxpayer.

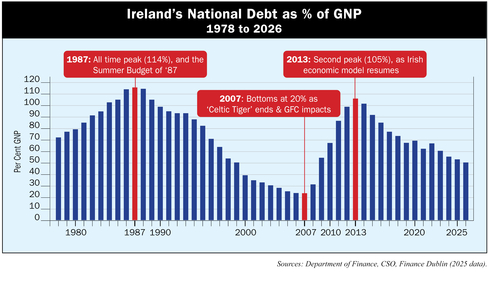

The latest figures from the NTMA show the national debt at just €217.9 billion, at the end of May, which brings, according to the metric of debt as a percentage of GNP/GNI published on the Finance Dublin debt clock page to below 50%.

This drop below 50% was previously seen in Ireland in 1999, when for a brief, golden era, 2000 to 2007, it remained below that.

If Departmental cash balances are factored out of the €217.9bn gross total, as they could be, the Net National Debt fell below €200bn to a post GFC crisis low of €188.7bn at the end of May. That stands at just 41% of the country’s current GNP.

Marking the start of the annual pre Budget season of speculation, leaks and negotiation via media that starts at this time every year, the T?naiste and Minister for Finance so far appears to be taking on board the positive data from the Exchequer returns - stating at the Economic Dialogue meeting in Dublin Castle in June that the economy “continues to demonstrate resilience and strength”.

And he seemed to also be in a mind to fuel expectations of such tax relief. Amongst his comments were the following: “Successive budgets have increased the point at which workers enter the higher rate of income tax, helping people keep more of what they earn. But we do need to do more”; “As we prepare Budget 2027, we will consider further increases in that threshold as a practical way of ensuring wage growth translates into higher take-home pay.” He also said the cost of childcare “remains one of the largest monthly expenses”.

He also remains on course to introduce an Irish SIA stating that “too many people save responsibly, and regularly, but feel locked out of investing and wealth creation”. As part of Budget 2027, we will make saving and investing more accessible and more attractive for ordinary households.”

On the SIA, the devil will be in the (tax) detail - as Irish investors contemplating a historically unprecedented new equity investment product are likely to be highly influenced by the tax consequences of their choices. Those considerations will be particularly acute in 2026 conditions with equity at record highs, making anything that suggests an annual levy on invested balances a big disincentive to prospective investors.

At the heart of that debate is a choice between an annual tax levy on invested balances (a ‘wealth tax’ model, as per Sweden’s ISK) or an income tax model, tax being paid on exit on gross (tax free) rolled up gains. This latter is the approach favoured in the Canadian (TFSA) and British (ISA) models familiar to Irish investors, and favoured by many in the financial services industry, including the Irish Banking & Payments Federation who presented a detailed study of the subject to the Government in May. |

|

|