| Financial services in an inflationary environment |

|

Inflation is back, and the big question now in the minds of monetary policymakers around the world is will its return be temporary? The uncertainty of this is reflected in all financial, securities and commodity markets this summer reflected in the volatile markets faced by asset managers, insurers, and other financial services providers in the first six months of this year.

As the global guessing game continues about the outcome, and its duration, as well as its medium term impacts, in terms, for example of permanently higher interest rates perhaps, we examine the possibilities and the potential impacts in the world of finance. |

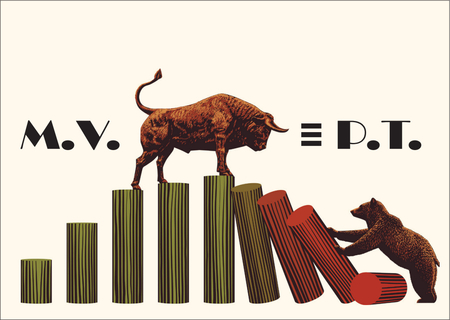

The graphic accompanying our cover story this month depicts one of the age old fundamentals of economic science – the “Quantity Theory of Money” summarised in an equation, variously labelled “the equation of exchange”, the “Fisher equation”, or the “Cambridge equation”, all of which encapsulate a fundamental reality variously described in writings that can be traced back for centuries, to the likes of David Hume, Adam Smith, and before.

In plain language, it says that the amount of money printed by the person with the authority to do so - in ancient times an emperor, and in more modern times a central banker - will tend to influence the overall price level, and in the long run, actually totally determine it, most likely. But there are nuances, notably the “V” part, and the “T” parts of the identity, or equation. (See this month’s GLOSSARY, page 11, for definitions).

These allow for the actions of other actors, such as trade unionists, (UK rail workers perhaps), corporations, or oil producers, or even warmongers, whose powers in their totality clearly are less direct, being diverse, uncoordinated, and random.

But even the central bankers, whose powers are more direct (they control “M”, the size of the actual money supply, and its ‘price’ (interest rates)) face uncertainties. That, in the face of the worst inflationary outbreak since the 1970s, is their current dilemma.

Their uncertainty is revealed in their actions since late last year, when it began to become apparent that the long suspected uptick in inflation that was to follow Covid was beginning to happen. That uptick was feared because of central bankers’ own actions and a consensus, that accommodative monetary policy was the correct (and expedient) path to follow when faced with the Pandemic in early 2020.

In different degrees, their actions have been dilatory, inconsistent, and to a degree uncoordinated. That is, up to recently (specifically this month), when a hawkish consensus has broken through.

This has been led by Jerome Powell, the chairman of the United States Federal Reserve, accompanied by the Swiss, who raised their policy interest rate for the first time in 15 years in a surprise move on 16th June saying that it was ready to hike further, joining other central banks in doing so.

These recent moves have been preceded by a growing awareness that decisive and early action was going to be needed, and that sharp rises in interest rates were going to be the only way to stop the inflationary outbreak.

An example of this was the interview given last month by one of the most eminent central bankers, the retired former governor of the Bank of England, Lord Mervyn King, who, as reported in last month’s issue of Finance Dublin, had moved decisively to the side of the hawks.

The American move from gradualism to hawkish, as exemplified by this month’s 0.75% hike has been swift.

Only a month earlier, the Fed Chair was still relatively dovish, a reputation he had earned since his accommodative stance in continuing QE during the Covid crisis, in effect underpinning the long bull market in US equities that followed the initial sharp downwards reaction in financial markets following the outbreak of the Covid pandemic in the first quarter of 2020.

Powell, first appointed by President Donald Trump in 2018, was reappointed by President Biden as Fed Chair in November 2022, but it was not until mid March 2022 that the Federal Reserve raised the Federal Funds rate, and then only by 0.25%. In May, it raised the rate again, this time be a slightly bolder 0.5%, but then, on June 16th, finally bit the bullet with a 0.75% hike, bringing the Fed funds rate up by 1.5%, and suggesting as he did so, that further rate rises might be anticipated, mentioning the number “0.75%” again in the process. | | Central Bank of Ireland Governor Gabriel Makhlouf |

Others, notably in the EU, UK and, least hawkish of all, Japan have followed, with lesser degrees of hawkish resolve as of June, illustrating, in this pattern that the United States is still in the lead position when it comes to world interest rate trend setting.

The consensus is taken with the following risks in mind:

- recession, unemployment; (particularly at risk in the UK, and in more sluggish EU economies)

- currency instability, within the euro zone

- stock market crash

- it may be ineffective, as much of the inflation is caused by supply chain disruption and the Ukraine war, i.e. supply side issues that monetary action in raising the price of money (interest rates) does not particularly affect.

The new hawkish monetary policy environment that has emerged this year will logically result in two possible main outcomes - (a) either it is successful in choking off the threatened world upsurge in inflation, sparked off by the likes of the latest inflation report in the UK, for example, of 9.1% inflation in May (11%+ in the RPI), or, (b) it fails, and, playing catch up, results in stagflation, one of the worst of all outcomes that central bank policymakers fear.

Finance and Financial Services

The detail of how the inflationary and interest rate story evolves in the rest of 2022 will be seen in microcosm in every industry sector, nowhere more profoundly than in the world of financial services, at least in its complexity.

We examine the potential impacts in major FS sectors, corporate treasury and finance, asset management and funds, and in insurance. In regard to the latter, the Governor of the Central Bank of Ireland, Gabriel Makhlouf, provided an analysis of the possible implications in his address at the annual lunch of Insurance Ireland in June.

He pointed out that high levels of inflation over a prolonged period would have more of an adverse impact on non-life (re)insurers (including health insurers) than life (re)insurers due to differences in the way claims are indemnified. This is because non-life firms typically indemnify the policyholder for incurred losses which are set in real terms, whereas life insurance claims are usually expressed in nominal terms.

Higher rates of inflation are already affecting the cost of settling some non-life claims due to rising labour and materials costs (for example, motor vehicle or property damage repairs), he said. “The impact of inflation on liability policies presents the greatest risk to profitability levels as claims may be settled many years after the premiums are paid. The adverse impact of inflation on some firms and on insurance costs may, however, be mitigated in part by the positive effects of higher interest rates on investment returns, alongside changes to the domestic personal injuries claims environment. This is because ultra-low interest rates particularly affect the limited number of life insurers offering longer term guaranteed products and act as a drag on non-life insurer profitability through the lower investment income they can generate”.

This reference to the differential impact on yields at different parts of the yield curve also illustrates the basis of the impact in other sectors, notably banking, where the traditional universal banking model is to borrow short and lend long, and in asset management.

Accordingly, some insurers, notably those in the life and pensions segments have been relatively less affected by stock market volatility in the US, most notably, where assessments of the impact on banks has been balanced by uncertainty over the conflicting forces of higher net interest earnings on banking balance sheets, against the potentially more devastating impact of defaults affecting loan balance sheets.

On this, the jury will remain out until clarification begins to emerge about the depth of the potential recession, and bear market, induced by the hawkish environment emanating from central banks.

When it comes to investment funds, the technical beginning of a bear market on Monday June 13th in the US (a purely technical market charts phenomenon) is always a point that will influence markets, certainly in the short term. This could point to a pause in the recent upwards march in Irish investment funds to, and beyond EUR 4 trillion in domiciled funds, and already it is resulting in changes in the composition of funds types and classes, with ETFs still holding strong, and increases in bond related funds for example.

As in all FS sectors, increases in market volatility are being regarded as opportunities for renewed focus on innovation, and further development of new strategies, for example, Northern Trust Ireland Country Head, Meliosa O’Caoimh observes that “our experience is that a number of asset managers that have historically been more active in the traditional rather than alternatives space, are now looking at launching private capital products at scale and at adding access to these funds for their clients to diversify their offerings”. Also the market volatility added to the Ukraine war are prompting other considerations, as IQ-EQ’s Mark Seavers, noted, in the light of the new sanctions on Russia “in future, asset managers may give a greater focus to human rights violations before they decide to invest in a country.”

In corporate treasury we asked Semin Soher Power, Head of Inflation Trading, Bank of Ireland Corporate and Markets and Eavan Coakley from Bank of Ireland’s Corporate and Institutional Treasury Solutions, (see blue panel), as well as Billy Quinlan, Head of Global Banking Ireland at BNP Paribas Corporate & Institutional Banking, see blue panel, to provide their assessments on corporate strategies in the light of the inflationary environment.

In corporate finance and corporate treasury, risk management and financing strategies will be revised in light of the new environment, most significantly having to take on board the increased possibility of higher positive interest rates at the longer end of the yield curve. In essence this will involve a judgement call by all engaged in long term corporate financial planning as to whether we are witnessing the ending of an unique period in world financial history – that of unprecedented low, and even negative interest rates – or whether all this hawkishness will, as must be hoped, merely be a blip in the medium term. |

This article appeared in the June 2022 edition of Finance Dublin.

|

|