|

|

Wednesday, 10th June 2026 |

| Forex pressure on Irish firms: euro sterling exchange rate outlook 2009 |

|

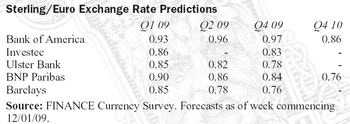

| With the Irish economy already on its knees the euro’s relative strength against sterling is a further hit to Irish competitiveness with nearly half of all exports from Irish-owned firms headed to the UK. In a FINANCE Magazine poll of leading corporate treasurers we ask for their outlook for the euro sterling exchange rate in 2009. |

One of the biggest exchange rate movements in recent times has occurred in euro sterling, which has traded from 0.67 to 0.98 in less than 18 months. The current strength in the euro relative to sterling is yet another crippling factor hurting the Irish economy. At the time of writing concerns over the British banking system has caused a further sell off of sterling with sterling falling by 2.8 per cent on January 20th to 93.25.

According to John Coffey at BNP Paribas says, ‘The current GBP weakness is disastrous for the Irish economy, which is already on its knees following the collapse of our property bubble & it’s ripple effect throughout the economy.’

‘Ireland’s ever increasing wage rates had made us uncompetitive even before the collapse in Sterling. Given the drop in global demand, Ireland’s imminent recession could be worse than anything that we have experienced in the 70’s, 80’s & 90’s.’ says Coffey.

Little respite for Irish businesses can be found in the forecasts of David Powell currency strategist at Bank of America who is bearish for sterling’s performance relative to the euro in 2009. He says, ‘The sharp loss of yield support for GBP as the BoE eases aggressively has weighed heavily on sterling.’

‘We expect the UK economic recovery to lag that of the Eurozone given the higher level of consumer indebtedness in the UK and the relatively larger dependence on the financial sector. In addition, the relatively larger UK current account deficit creates a negative back drop for sterling. As such, we expect the pair to peak around parity in 1Q 09 before EUR/GBP faces a sustainable decline.’

Other contributors to the survey have suggested that the outlook for the eurozone is bleak and pointing to a relative fall in the euro providing some relief for Ireland’s export sector.

David Page of Investec says ‘The risks of an appalling slowdown in the Eurozone economy are clearly growing. We believe Eurozone rates will continue to ease, almost as much as in the UK. We thus see sterling’s already very competitive level of the exchange rate as sufficient and see a modest pace of improvement across this year and next as the UK’s current account deficit swings back into surplus.’ He explains the rise in euro-sterling �0.98 as being driven by ‘’thin holiday markets and a misperception about the likely outlook for Eurozone interest rates, guided by an overly optimistic set of Governing Council remarks in the wake of December’s easing.’

Ciaran Kane head of treasury at Barclay says their predictions, found in the table, are predicated on a severe UK recession being priced into sterling i.e. the main factor behind recent weakness. He says, ‘We expect the Eurozone to enter recession in 2009 - we don’t believe that this is fully priced into the Euro currency. In addition, the UK economy will begin to recover sooner than the Eurozone which should also be sterling supportive.’

‘The latest economic numbers out of Germany have been nothing short of alarming and included a second consecutive 6 per cent monthly plunge in factory orders and a staggering 10 per cent collapse in exports. Industrial production numbers from France and Spain were also extremely poor, confirming that the escalating weakness is not simply a German phenomenon,’ says Simon Barry, senior economist at Ulster Bank Capital Markets.

Barry says, ‘The UK economy is certainly not in good shape, but a foreign exchange rate is a relative price. Last year, traders were firmly focused on the weakness in the UK and what that means for interest rates there. The price action early this year suggests that escalating weakness in Europe is, rightly in my view, a greater concern. The implication is that the ECB is behind the curve and has much further to go in getting euro zone rates down.’

‘The phrase ‘benign neglect’ seems particularly appropriate as there is no doubt that the UK authorities, especially the Bank of England realised, at an early stage, that a serious downturn was on the way and that significant currency weakness might help mitigate the economic problems to come by assisting the export sector of the UK economy,’ says Ian Stannard, senior currency strategist at BNP Paribas.

‘Much of the UK’s economic weakness is now factored in and that the next negative shock will come from Europe where the market continues to underestimate the impact of the global slowdown and the financial crisis on the Eurozone economy,’ says Stannard.

‘We expect substantial further easing in the coming months with the refi rate reaching 1.0 per cent in Q2. We expect a melt down in growth with contractions in excess of 1.0 per cent q/q in both Q4 2008 and Q1 2009,’ says Stannard.

‘Another concern for the euro is the level of government bond issuance in the coming year. 2009 European government net bond supply should increase 54 per cent increase in 2009. The rating agencies are putting sovereign ratings in Europe under greater scrutiny (Spain, Ireland & Greece, in particular) and this could make issuing this extra supply more difficult & increasingly expensive,’ says Stannard.

‘Bond spreads over Germany have widened considerably - to new highs, in some cases. This spread widening may reduce foreign investor interest in eurozone assets, thus putting the euro under pressure,’ he says. |

|

|

|