| Funding diversification is a must for Irish companies |

|

| 2013 is proving to be a challenging year for companies as they manoeuvre through tepid and uncertain economic growth, recessionary conditions in the Eurozone, debt ceiling and spending concerns in the US, global austerity, and unprecedented monetary easing by central banks. Tony Golden managing director and Louise O’Mara director of Citi Banking Ireland look at the importance of funding diversification for Irish companies. |

While the health of the global banking sector has improved, higher capital requirements and regulatory and macroeconomic uncertainty continue to constrain the availability of bank credit for many companies. This effect is exacerbated in Europe where bank deleveraging may contract credit availability by 2.5% in core Euro countries and by almost 18% in peripheral Eurozone over the quarters preceding the end of 2013 (IMF estimates). | | Tony Golden |

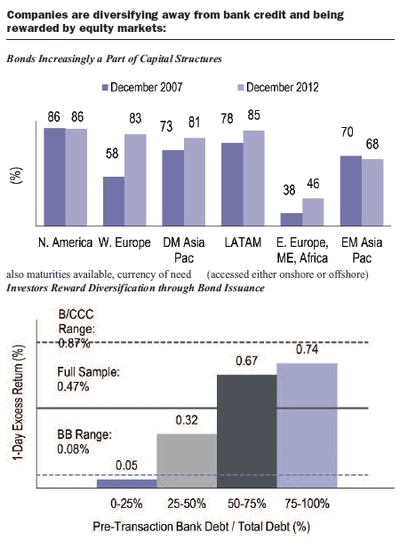

In light of these pressures, Global companies including the large Irish companies are proactively diversifying their funding sources. Smaller and highly levered companies are now accessing the bond markets in most regions of the world. The trend is especially pronounced in Western Europe where 83% of such companies now have bonds in their capital structure, compared to only 58% in 2007. Companies are also improving their financial flexibility by extending debt maturities and issuing debt in multiple currencies - 71% of Western European companies now have debt denominated in multiple currencies versus 57% in 2007.

Golden says “the funding diversification imperative is particularly strong for non-investment grade issuers in light of Basel III requirements that impose higher risk weightings for such issuers. Along with reduced credit availability, pricing for non-investment grade loans could increase by 100bps assuming a 10% bank ROE threshold. Not surprisingly high yield firms heavily reliant on bank debt are having to pay a premium. Equity investors of non-investment companies have responded positively when these firms have issued bonds to repay bank debt”.

Large Irish companies have good access to bond markets

2013 started strongly across all debt markets, allowing Irish borrowers good access to funding and flexibility to choose a market of preference. The decision on which market to use is based on a number of factors, including price of course, but also maturities available, currency of need (especially if there’s a preference to avoid swapping), size requirement and more strategic considerations such as investor diversification. On price, the ‘cheapest’ market has been unclear, since corporates assess funding on different bases: some fixed, some floating and not all necessarily in Euro. On investor diversification, there have been opportunities for corporates to ‘take their pick’ from mainstream markets, with each of US$, EUR and GBP having good reasons to be considered, and less mainstream markets such as Renminbi (accessed either onshore or offshore) opening up genuinely new investors for corporates. | | Louise O'Mara |

A number of Irish corporates took advantage of capital markets to raise finance earlier in the year. Some notable transactions include Ardagh USD 1.6BN High Yield Bonds the largest European high yield deal completed in the last two years, Smurfit EUR 400MM Senior Secured Notes and Digicel USD 1BN Bond Issuance. Golden points out ‘larger Irish corporates often have significant US businesses so that market can make sense, and is also usually comfortable at 10-yr maturities, although this year 10yr has often been available in Euro too, as those investors sought yield and conditions were favourable. Longer Euro was very much a 2013 phenomenon as Euro “sweet spots” are normally shorter, e.g. 7-8 years, depending on rating’.

In addition to diversifying funding sources, liability management through the repurchasing of shorter maturities and extending the maturity profile of borrowings should continue to be of high priority. O’Mara says ‘The combination of low interest rates and a relatively flat yield curve makes issuing longer maturities an attractive proposition in advance of potential increases in long-term rates and a steepening of the yield curve’.

The last 6 weeks or so has brought more volatile conditions, especially following the FOMC in the US stating that QE would come to an end, at some point, if the underlying economy was judged to be strong enough. The fear that this will lead to rate rises has led to an increase in new issue concessions in the bond markets; simultaneously we are reminded by events in Portugal that European related risks are still present and events in Egypt keep geo-political risks elevated.

O’Mara adds “A little bit of volatility is always welcome as it forces everyone to be alert and sharpen their risk perceptions. Although the market is stabilising investors are still watching for clues regarding the future path of QE from the Fed and signs of stabilisation in GDP growth and credit conditions in China.”

Further into 2013, O’Mara believes ‘that the investment landscape will continue to be dominated by several key themes with a reversal in global liquidity the key underlying concern. Investors are likely to be increasingly concerned with the start of the Fed QE tapering causing volatility in rates across developed markets and also contributing to an underperformance in emerging markets. For Irish corporates who have completed funding they can breathe easy. For those with funding still to do, it is likely to prove more expensive than it would have been earlier in the year. This should be kept in context that even though more expensive, funding costs are significantly lower than the worst years of the crisis’.

As economic conditions recover, inflation and the cost of capital will rise. In addition, Basel III rules will tighten credit availability for certain borrowers. Irish companies will continue to diversify their funding sources and push debt maturities further out through long-dated capital market issuance while capital market and long term funding costs remain highly favourable.

Citi has a significant Corporate and Investment banking business in Ireland. We provide a full suite of treasury services to over 300 clients in Ireland. |

Tony Golden is managing director and Louise O’Mara is director of Citi Banking Ireland.

|

|

|