| Ireland topped eurozone GNP growth in 2013, with 3.4 p.c. rate |

|

The release of the first official estimates for GNP and GDP for Ireland from the Central Statistics Office earlier this month met with some bemusement amongst commentators on the economy, as the figures showed that Ireland recorded a growth rate in 2013 of 3.4 per cent in volume terms - close to the highest in the developed world.

A remarkable fact about this is that the growth was recorded in GNP rather than GDP - a measure of the real economy that is more reliable than the more commonly employed GDP figure. So radically divergent the two measures have become now means that if we were to continue to judge the economy by GDP data alone we would have to conclude that the economy has remained in a sideways recession since 2011, and that 2013 saw no economic progress at all.

There are particularly good reasons why analysts of the Irish economy should rely on the GNP (or ‘GNI’) figures rather than the GDP figures to gauge the progress of the economy as it exits its great recession as we may be in danger of underestimating both the strength of the recovery, and its causes.

It also raises the intriguing possibility of growth rates returning potentially to levels unseen since the ‘Tiger’ years. Even the most Keynesian of ‘Keynesian’ economists (who tend to see spending by consumers or government as the main driver of growth (rather than investment, and supply side factors)) are having to question the understanding of the Irish economy’s performance in the light of the false readings of the true growth in the economy conveyed by a reliance on the quarterly GDP statistics.

Because of the openness of the Irish economy and its reliance on FDI and exports for growth (and jobs) the contrast between GDP and GNP is more pronounced than in most economies. As a result, more than elsewhere, analysts of Irish growth need to pay particular attention to the GNP rather than the GDP as the indicator of the true wealth and income of citizens resident in the country. GDP in 2013 fell by 0.3 per cent, and shrank in the final quarter, due largely to a decline in what the CSO called ‘net exports’, reflecting the ‘patents cliff’ phenomenon whereby exports of pharma products coming off patent have been reduced in value, squeezing gross export figures as a result. The Central Statistics Office defines the Gross National Product (GNP) as "the sum of GDP and net factor income from the rest of the world, which is the difference between investment income and labour income earned abroad by Irish residents and companies (inflows) and similar income earned in Ireland by non-residents (outflows)". Therefore, the GDP figures only take account of one side of the balance sheet, and thus don’t track the equal and offsetting decline in net factor income outflows on the other side. But when account is taken of the changes in net factor income, as the GNP figures do, the figures show that a strong recovery was underway in 2013, and which has been intact since the first quarter of 2012.

This is shown in the chart at the following link on the CSO website: Quarterly GNP Figures While exports have been squeezed, by the 'fiscal cliff', there was an equal and offsetting reduction in net factor income outflows, profits and rents, which are believed to correspond to the decline in exports by major multinationals. The GNP data have shown that the economy has been improving steadily since Ireland's double dip recession of 2009-2011. This accords with most anecdotal experience, and with data for employment, and, another key indicator, income tax revenues. By contrast, the chart of GDP by quarter provides an inaccurate impression due to the net factor income complications, seen at this link: Quarterly GDP Figures

The GDP data would suggest that Ireland has been in a sideways recession since 2011, and indeed that it continues on a downward trajectory - just not in accord with a host of real indicators, such as employment figures.

Are there also policy implications to the story of the GDP and GNP figures? Those commentators emphasizing the 'austerity' story, for example the leading 'Keynesian' (so called) economist, Paul Krugman, that Ireland could not possibly emerge from the bailout, or restore its economy to health on foot of its 'austerity' measures or its failure to rely on public expenditure to kick start or pump prime the economy, are inclined to de-emphasise the GNP figures.

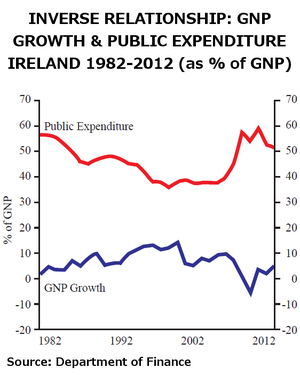

This is because the latest GNP figures reflect (again) the uncomfortable reality for 'Keynesians' that there is historically an inverse relationship between Public Expendtiure and GNP growth in Ireland. This, as the chart on this page shows, has proven to be the case in the past 30 years. What's also at odds with the 'Keynesian' diagnosis is that the pattern is again showing itself. The causative link, ‘supply side’ economists say, is that falling public expenditure translates itself into rising private expenditure, due: a) to rising confidence by taxpayers - i.e., the gainfully employed (that they will see an end to tax impositions), and b) a displacement effect - less tax leaving more money in the hands of earners to spend on goods and services, (and indirect taxes).

Article in the March 2014 edition of Finance Dublin: Hidden Ireland: The GNP Recovery 2012-2014 |

|

|